Investor Strategy Guide

Fix-and-flip works best for investors seeking short-term profits, while buy-and-hold is ideal for building long-term cash flow + wealth compounding. The real decision isn’t “which is better?” — it’s which fits your timeline, deal access, and stress tolerance.

Flip focus

Speed + Margin

Execution matters most

Hold focus

Cash Flow + Equity

Consistency wins

Best first move

Run numbers

Before you commit

Fast rule of thumb

If you hate surprises and prefer predictable progress, buy-and-hold tends to fit better. If you like projects, deadlines, and problem-solving (or have a strong GC + systems), flipping can be a great business.

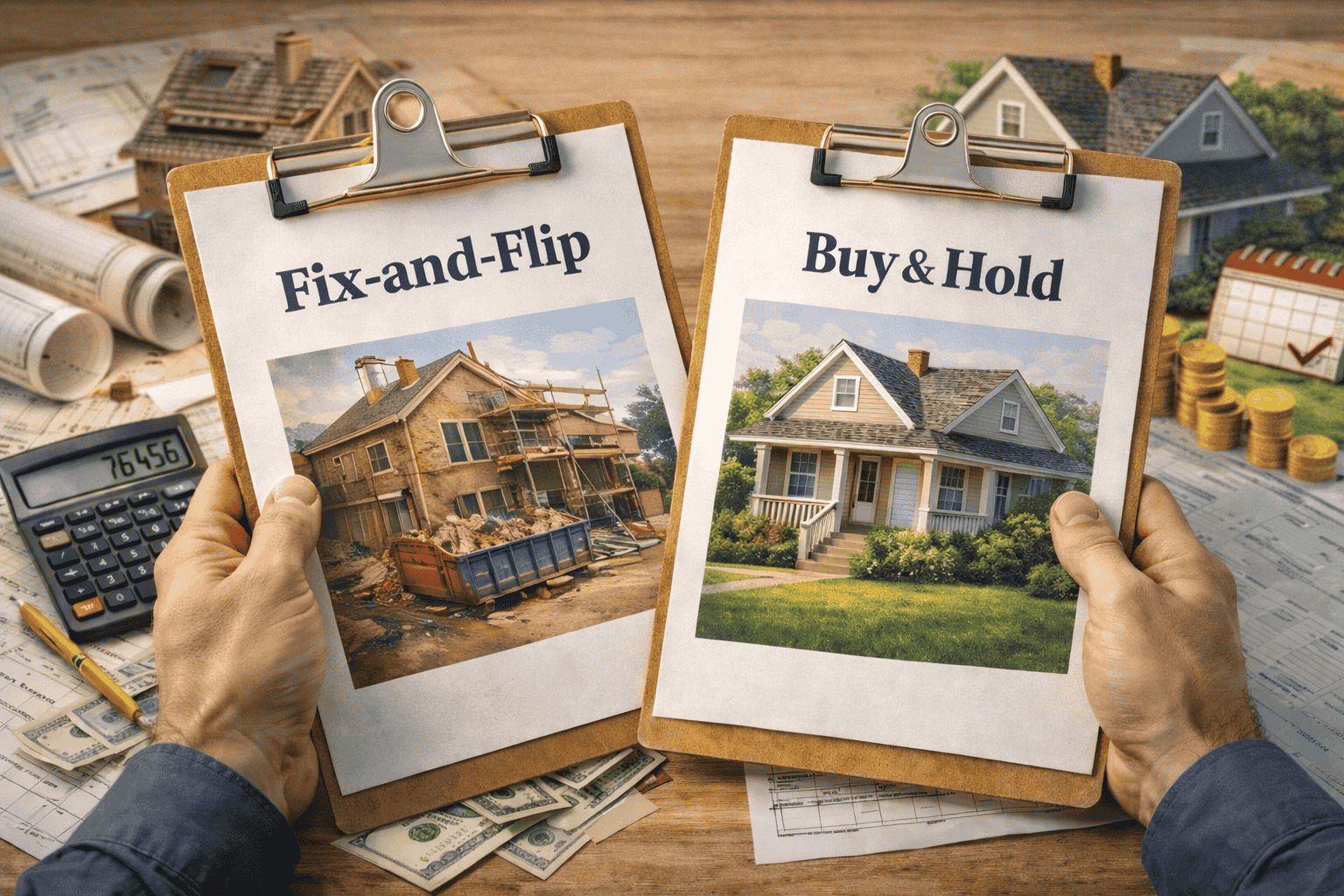

Flip vs Hold at a glance

Choosing between flipping and holding comes down to what you want most: a quicker exit or a longer runway.

Fix-and-flip

- Short-term, active investing built around renovation + resale

- Higher risk, faster potential payout per deal

- Profit depends on scope control + timeline

Buy-and-hold

- Long-term, more passive investing built around renting + equity growth

- Lower volatility, steadier wealth-building over time

- Returns stack through cash flow + paydown + appreciation

What is a fix-and-flip strategy?

A fix-and-flip strategy involves improving a property and selling it quickly for a profit. In practice, you buy an undervalued home, complete targeted renovations, then resell into the retail market. The best flips aren’t “HGTV makeovers.” They’re disciplined projects with tight scopes, clear comps, and a realistic timeline.

Key success driver

A time-sensitive plan that keeps contractors, inspections, permits, and listing prep moving without costly pauses (where holding costs quietly eat your margin).

Helpful reads

If you want the “lender view” of flips, these are strong next steps:

- Fix & Flip Loans in South Carolina (requirements + timeline)

- How to Fund Your First Fix & Flip

- How to Create a Fix & Flip Budget

What is a buy-and-hold strategy?

Buy-and-hold focuses on earning rental income and building long-term equity. Your return comes from monthly cash flow, loan paydown (tenants help pay the mortgage), potential appreciation, and tax dynamics like depreciation (talk with a tax pro for your situation).

Why rentals scale well

You’re not forced to “hit a resale window.” Instead, you build a portfolio that can handle rate shifts and market noise because the strategy is anchored by monthly demand for housing.

Where DSCR fits (and why investors use it)

Many rental investors use DSCR loans to qualify based on the property’s rent vs. payment (instead of personal DTI). That can make scaling easier — especially if you’re self-employed or already own multiple properties.

Profit potential: short-term vs long-term returns

Fix & flip profit model

Flips usually produce a one-time profit at resale. Your margin is sensitive to a few numbers that must be right (not “close enough”): purchase price, rehab budget, and market conditions during the listing window.

- Purchase price: did you buy below market or at market?

- Rehab budget: labor, materials, surprises, change orders

- Market: days on market, buyer demand, rates

Buy-and-hold profit model

Rentals stack multiple return channels — which is why buy-and-hold builds wealth so reliably over time.

- Monthly cash flow: rent minus expenses

- Equity growth: principal paydown

- Appreciation: market growth + strategic upgrades

- Tax dynamics: can be meaningful (scenario-specific)

Reality check

Flips can outperform renting in a hot cycle — but they punish small mistakes. Rentals may feel slower early on, but they reward patience and repeatability.

Risk level & market sensitivity

Flip risks

Sharp + immediate

Overruns, delays, market shifts, holding costs

Hold risks

Slow + persistent

Vacancy, maintenance, tenant ops, compliance

Holding costs are the silent killer (for flips)

Every extra week adds interest, insurance, utilities, taxes, and “life happens” expenses. Build a buffer into the timeline and budget so your profit isn’t depending on perfection.

Financing differences & capital requirements

Your financing options often determine which strategy fits best. The cheapest rate isn’t always the best product — the right loan matches your timeline and exit plan.

Fix & flip financing is built for speed

- Short-term loans designed for renovation + resale

- Higher rates/fees than long-term mortgages (in exchange for flexibility)

- Fast closings when timing matters

If you’re investing in South Carolina, start here: Fix & Flip Loans in SC.

Buy-and-hold financing is built for cash flow

- Longer terms that support rental cash flow

- Qualification may use personal income (conventional) or rent (DSCR)

- Better fit for portfolio building

Want the rental path? Use: DSCR loan details + DSCR Calculator.

Pro tip: the hybrid path (BRRRR)

Many investors combine both strategies through BRRRR (Buy, Rehab, Rent, Refinance, Repeat): fix-and-flip-style funding for the purchase/rehab, then a DSCR refinance to stabilize as a rental. See: BRRRR Strategy with Fix-and-Flip + DSCR.

Time commitment & experience level

Flipping rewards operators

If you enjoy project management (or have a trusted GC + tight systems), flipping can be a great business. Without that, it becomes a stressful second job — and timelines slip.

Rentals reward consistency

Buy-and-hold can be more passive (especially with property management), but it’s not “set it and forget it.” Great landlords track expenses, plan capex, and screen tenants carefully.

Which strategy is right for you? A simple decision framework

Choose fix-and-flip if you:

- Want quicker returns and can handle variability

- Can manage renovations, contractors, and timelines

- Understand resale comps + buyer demand in your market

- Prefer profit events over steady monthly income

Choose buy-and-hold if you:

- Want long-term income and wealth compounding

- Prefer stability over speed

- Plan to scale into multiple doors over time

- Want financing that can qualify based on rent (DSCR)

Ask yourself these 4 questions

- Timeline: do you need profit this year, or are you building long-term?

- Stress tolerance: how do you handle surprises + deadlines?

- Deal access: do you consistently find discounted properties with margin?

- Operator skill: do you have a GC + systems that actually hit timelines?

Can investors use both strategies?

Yes — many investors combine both to diversify income and keep capital moving. A common pattern is: flip for chunks of capital + rentals for stability.

A clean way to blend both

Use flips selectively when you find deep margin deals, and place the best properties into your long-term portfolio. If you like the “buy, rehab, rent, refi” model, start here: BRRRR Strategy with Fix-and-Flip + DSCR.

Frequently asked questions

Is fix-and-flip more profitable than buy-and-hold?

Flips can produce faster profits per deal — but they’re sensitive to budget, timeline, and market shifts. Buy-and-hold typically builds long-term wealth more reliably through cash flow, equity paydown, and appreciation.

Which strategy is better for beginners?

Buy-and-hold is often more beginner-friendly because you’re not forced to sell on a deadline. Flipping can work early if you have strong support (GC + systems) and conservative numbers.

Does location matter when choosing between flipping and holding?

Yes. Resale demand, DOM, rent demand, and insurance/tax dynamics all change your risk profile. The best strategy is the one that fits the neighborhood trends and your execution plan.

Can I refinance a flip into a rental loan if I change my mind?

Often, yes — depending on the property, seasoning rules, and rental income. Many investors use DSCR refinancing to stabilize a renovated property as a long-term rental.

Helpful read: DSCR Refinance in South Carolina.

Which strategy requires less upfront cash?

It depends on the deal and financing. Flips can require more short-term liquidity (reserves + rehab + buffers). Rentals require down payment/reserves, but costs are usually spread over time.

Bottom line

Fix-and-flip and buy-and-hold can both work when they match your goals and your personality. Flips emphasize speed + execution. Rentals reward patience + consistent management. Before committing, pressure-test your numbers and align financing to your exit plan.

Want fast clarity? We’ll help you map the cleanest funding path for your strategy — and tell you what matters most to get approved.

Disclaimer: This content is for educational purposes and doesn’t constitute financial, legal, or tax advice. Program guidelines and pricing can change and vary by scenario.