South Carolina Refinance Guide

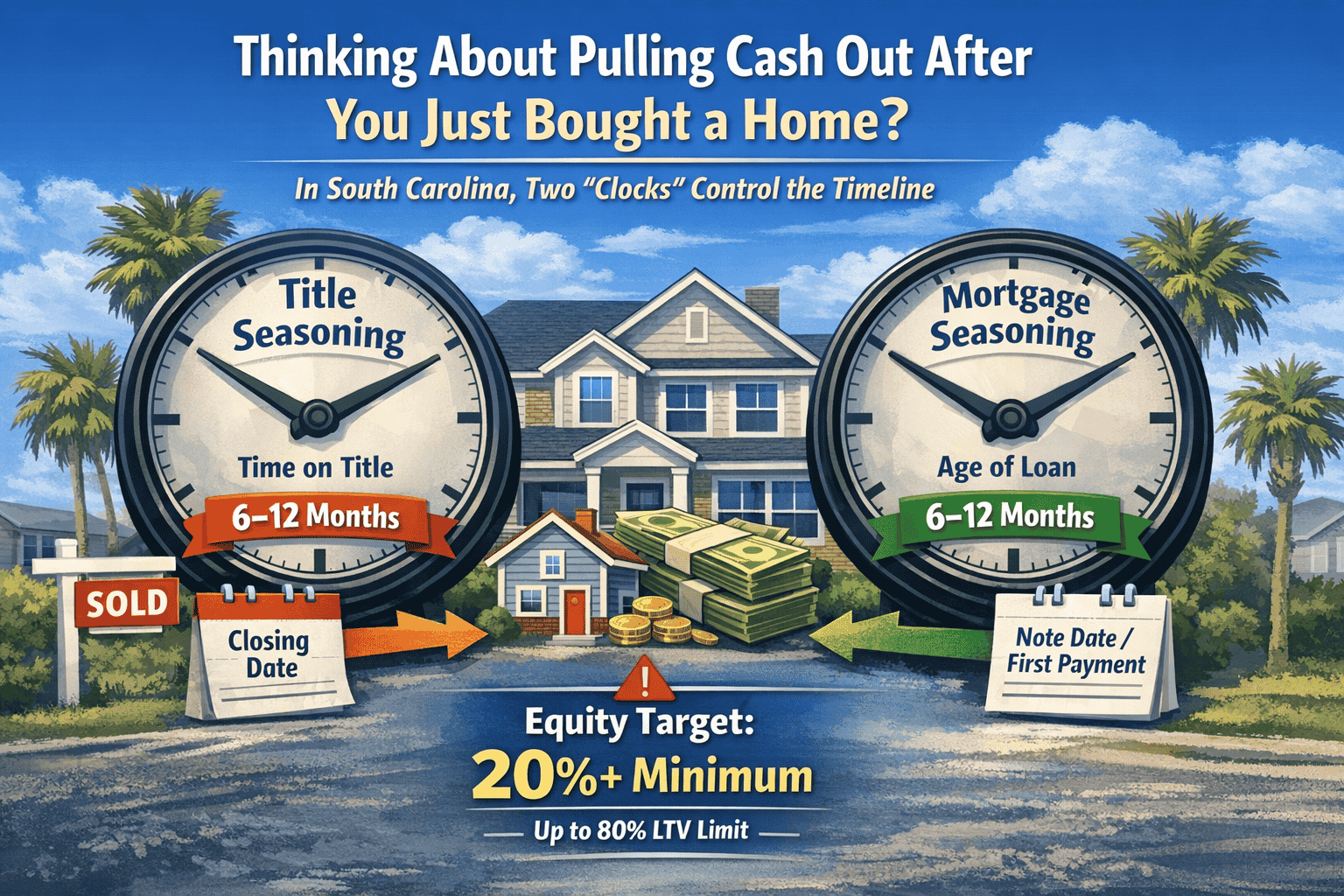

Thinking about pulling cash out after you just bought a home? In South Carolina, the “real” answer is usually about seasoning + equity — and the timeline can be 6 to 12 months depending on the program and lender rules. This guide breaks it down so you know exactly what controls the clock, what equity you need, and how to plan your next step.

Typical timeline

6–12 months

Depends on ownership + loan seasoning

Common equity target

~20%+

Many cash-out caps are near 80% LTV

Big “gotcha”

Seasoning

Title vs. mortgage note date

Quick answer: how soon can you do cash-out after buying in South Carolina?

Most people hear “6 months.” The real planning window is often 6–12 months.

Conventional cash-out is frequently limited by ownership/title seasoning and, in many cases, the age of the mortgage being paid off. FHA and VA can follow different seasoning rules, and lenders can add overlays on top of program guidelines.

Typical ranges you’ll see

- Conventional: often 6–12 months depending on seasoning rules and lender overlays

- FHA cash-out: commonly longer (often around a year) depending on program + lender policy

- VA cash-out: commonly tied to a seasoning concept (days since first payment + number of payments)

What you should do first

- Figure out which “clock” applies to your situation

- Estimate equity using a conservative value range

- Run a payment snapshot so you don’t get surprised

What a cash-out refinance is (in plain English)

A cash-out refinance replaces your current mortgage with a new loan that’s larger than what you currently owe. The new loan pays off the old loan, and the difference comes back to you as cash (minus closing costs).

Equity basics

Home value − Mortgage balance = Equity

Cash-out lets you tap a portion of that equity while keeping a required amount in the home.

Quick reality check

Cash-out is powerful — but it’s still a mortgage. Your home is collateral, and the new loan can increase your payment depending on the rate, balance, and term.

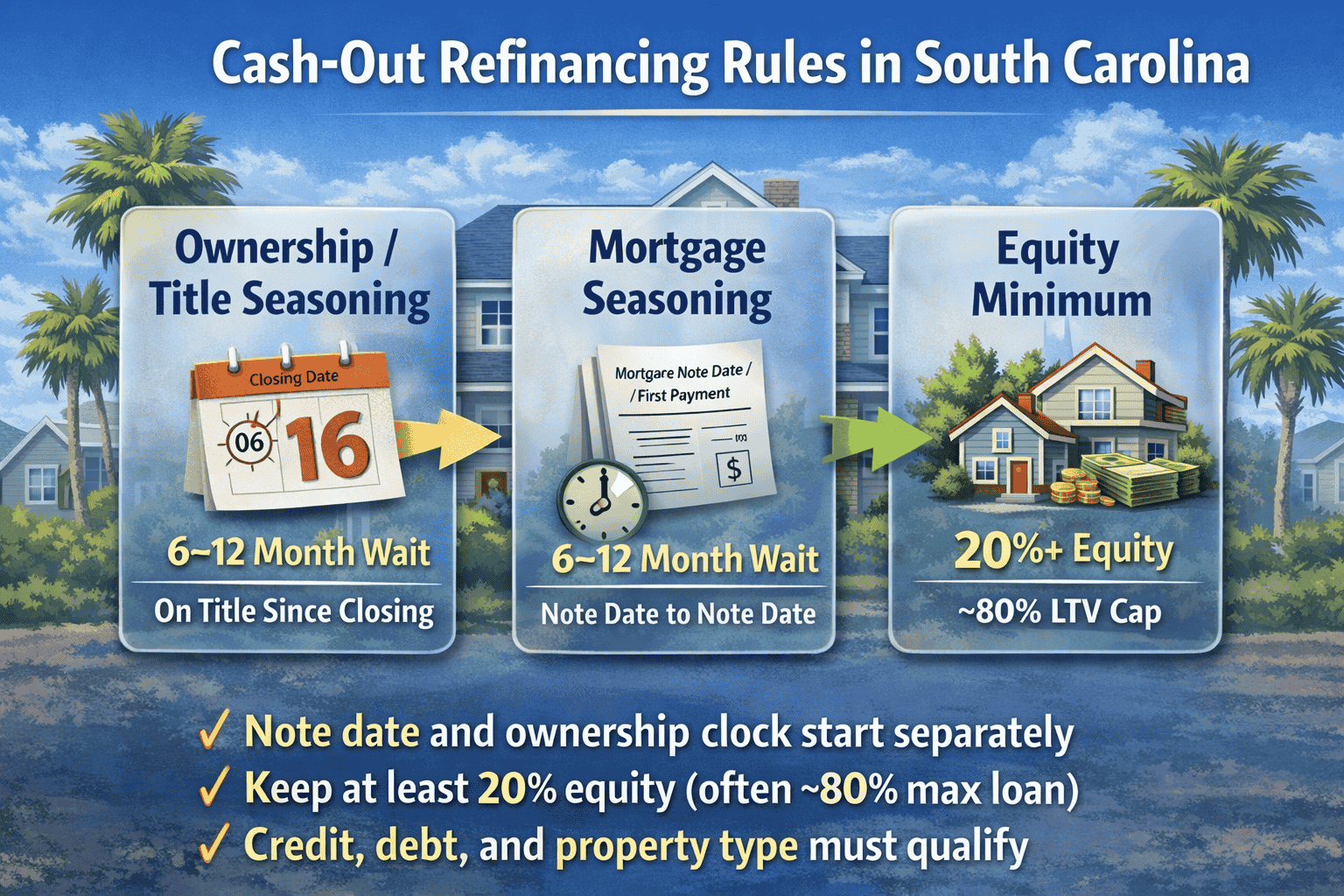

What controls “how soon” (most people miss this)

Timing usually comes down to two separate seasoning requirements. This is why one person can refinance quickly while another has to wait — even if both bought around the same time.

Clock #1: ownership / title seasoning

Some programs require at least one borrower to have been on title for a minimum period before a standard cash-out is allowed. This is the reason “6 months” gets quoted so often.

Clock #2: mortgage seasoning

In many situations, there’s also a requirement tied to the loan being paid off (think “note date to note date”). So you can hit 6 months of ownership and still not qualify if the underlying mortgage hasn’t seasoned enough.

Fast checklist (takes 60 seconds)

- ✅ What date did you take title? (closing date)

- ✅ What’s the note date on your current mortgage?

- ✅ When was your first payment due?

- ✅ Is this a primary residence, second home, or investment property?

South Carolina specifics: what’s different here?

South Carolina typically follows standard federal and program guidelines for cash-out refinancing. You won’t find a unique statewide “cash-out waiting period” rule — most of your timeline comes down to your loan program and lender overlays.

Local market factor that actually matters

The big SC variable is appraised value. Some neighborhoods move faster than others. If your appraisal comes in higher, you may hit equity targets sooner. If it comes in low, your cash-out amount can shrink quickly.

Equity rules: how much do you need?

Many cash-out refinances require you to keep a meaningful equity cushion. A common guideline is that your new loan amount can’t exceed about 80% of the home’s value on a primary residence (rules vary by program and property type).

Simple cash-out example

- Appraised value: $400,000

- Current mortgage balance: $280,000

- 80% max loan: $320,000

- Potential cash-out (pre-costs): $40,000

Your final cash-out depends on closing costs, rate, and program limits.

How to estimate equity without guessing

- Pull 3–5 recent comparable sales nearby

- Use a conservative value range (low / mid / high)

- Subtract your estimated payoff

- Apply an 80% cap to see what’s realistically available

Credit, DTI, and eligibility (the part that actually approves the loan)

Seasoning and equity get you in the door. Underwriting is what closes it. Here are the big items lenders review for a cash-out refinance:

Credit score

Conventional cash-out often starts around the low-600s, but stronger credit usually means better pricing and fewer restrictions.

Debt-to-income (DTI)

Lenders look at total monthly debts compared to gross income. Lower DTI typically improves approval odds and pricing.

Property type

Primary homes are typically most flexible. Second homes and investment properties often have tighter LTV and reserve requirements.

Pro tip

If your goal is cash, your fastest path is often: know your seasoning date + confirm equity + run a payment snapshot. That prevents wasted applications and surprise denials.

Can you do it earlier than the normal waiting period?

Sometimes you can refinance earlier, but it’s usually not a true cash-out refinance. Early refinances tend to fall into “rate-and-term” or specific corrective scenarios.

More common early options

- Rate-and-term refinance (change rate/term, roll costs)

- Corrective refinance (fix an issue with the original loan)

- Title/ownership changes (specific qualifying situations)

What’s usually not possible early

- Pulling significant cash from equity without meeting seasoning rules

- Bypassing appraisal and LTV caps

- Skipping lender overlays (they still apply)

Step-by-step: cash-out refinance process in South Carolina

Confirm your seasoning dates

Check your closing date, note date, and first payment date. This tells you which timeline applies.

Estimate equity (conservatively)

Use nearby sales to get a value range, subtract payoff, and apply a realistic LTV cap.

Run the payment snapshot

Make sure the new payment fits your budget, especially if rates are higher than when you bought.

Compare lender quotes

Rates and costs can vary. Compare APR, lender fees, and required reserves — not just the headline rate.

Appraisal + underwriting

Your appraisal confirms value and your final cash-out amount. Underwriting confirms income, assets, and eligibility.

Close and receive funds

After signing, the new loan pays off the old loan and your cash-out proceeds are disbursed per closing rules.

Benefits and risks (so you don’t regret it later)

Benefits

- Often lower cost than credit cards or personal loans

- Can fund renovations, debt payoff, or major life expenses

- One payment instead of multiple high-interest payments

Risks & considerations

- Higher balance may increase your payment

- Resetting the term can increase lifetime interest

- Your home is collateral — missed payments have real consequences

- Appraisal can limit cash-out if value comes in lower than expected

Best practice

If you’re cashing out to pay off debt, make sure the plan includes how you’ll avoid rebuilding the balances. Cash-out works best when it’s paired with a clear strategy.

FAQs

How soon can I do a cash-out refinance after buying a home in South Carolina?

Many borrowers plan around a 6 to 12 month window. The exact timing depends on your program, lender overlays, and whether the seasoning requirement is based on title, the mortgage note date, or both.

Can rising home values help me qualify sooner?

Appreciation helps with equity, but it doesn’t automatically waive seasoning rules. The appraisal is what confirms value and supports your final cash-out amount.

Does South Carolina have a special law that changes the waiting period?

South Carolina generally follows standard program and federal lending guidelines for timelines. The main “differences” are local market values and lender overlays.

Can I cash-out refinance an investment property in South Carolina?

Often yes, but investment properties typically have tighter requirements (lower max LTV, stronger credit/reserves). The easiest first step is confirming value + payoff + eligibility for your specific property type.

Disclaimer: This article is for educational purposes only and does not constitute financial or legal advice. Mortgage guidelines and lender overlays can change. Talk with a licensed loan professional to confirm eligibility and terms for your situation.