South Carolina Refinance Guide

South Carolina homeowners—from Charleston’s historic neighborhoods to Greenville’s fast-growing communities—often ask the same question: “How much equity do I need for a cash-out refinance?” The short answer is usually about keeping a cushion after you pull cash out. This guide breaks down the LTV rules, equity math, and the factors that can change your number.

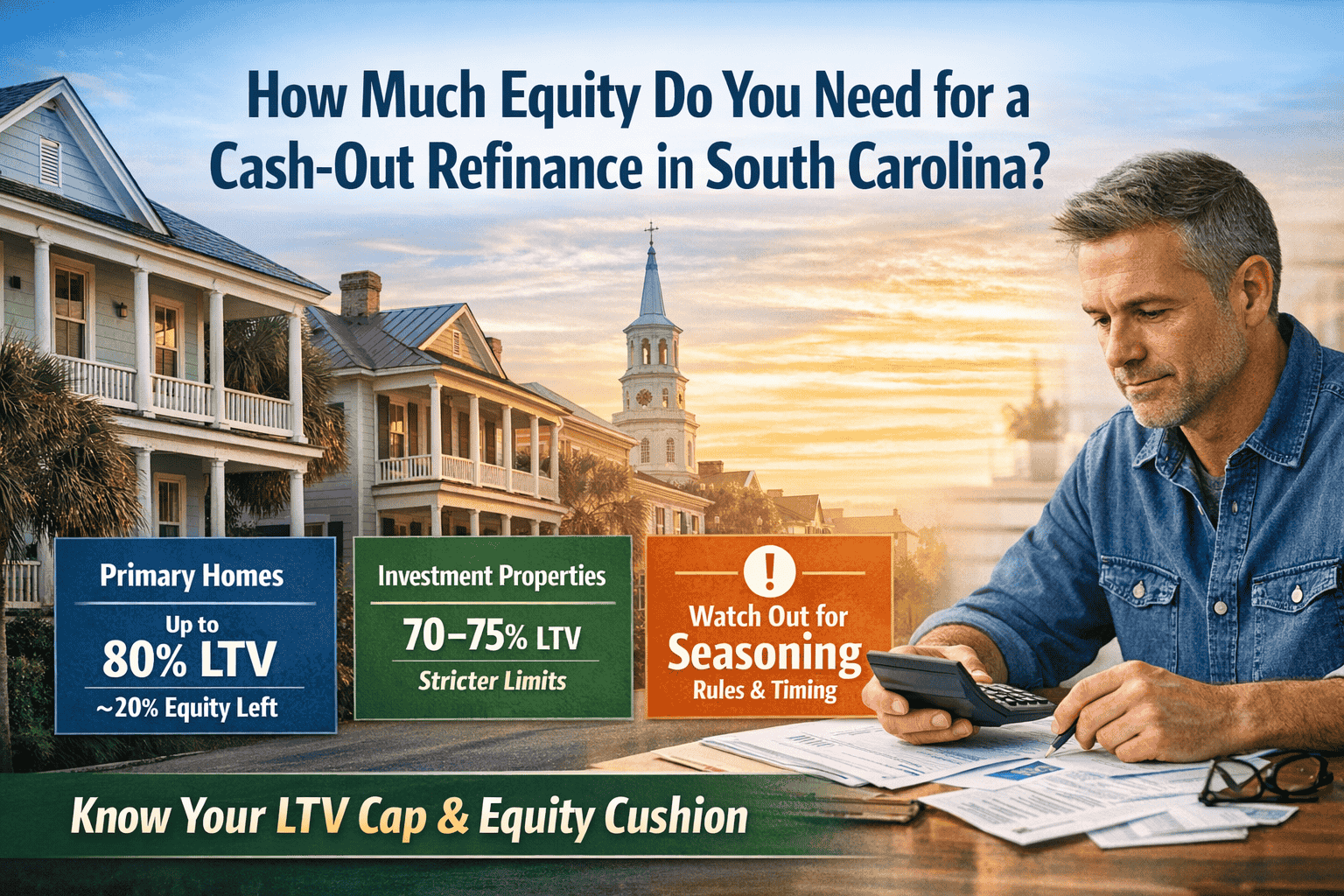

Common max for primary homes

~80% LTV

Often means keeping ~20% equity

Investment property caps

~70–75% LTV

Stricter because risk is higher

Big “gotcha”

Seasoning

Title + mortgage note timing matters

Quick answer: how much equity do you typically need in South Carolina?

Most borrowers plan around keeping ~20% equity.

Many borrowers qualify for a cash-out refinance when they can keep about 20% equity in the home after the refinance. In practical terms, that often means the new loan amount is capped around ~80% of the home’s appraised value for a 1-unit primary residence (program rules and lender overlays can vary).

Why lenders care about your “equity cushion”

Lenders aren’t just looking at what you can borrow—they’re looking at what happens if values dip or expenses rise. Keeping equity in the home protects you and the lender, especially in markets where values can swing.

What the equity cushion does for you

- Equity cushion helps you avoid being “stuck” if values soften.

- Lower risk often means better approval odds and better pricing.

- Investment properties usually require more equity than primary homes.

What is a cash-out refinance?

A cash-out refinance replaces your current mortgage with a new one for a higher amount. The old mortgage gets paid off, and you receive the difference as cash (minus closing costs).

- New mortgage replaces the old one

- Cash is typically received at closing

- New rate/term can be different from your current loan

What it’s commonly used for

- Home improvements (kitchens, roofs, additions)

- Debt consolidation (when it truly improves your overall plan)

- Buying another property or funding a down payment

- Major life expenses (tuition, medical, emergency reserves)

Tip: For investors, cash-out can be a strategy—just make sure the new payment still fits your cash flow goals.

Important

You’re turning equity into debt. If you pull cash out, your loan balance goes up—so the goal is to use the funds in a way that improves your overall financial position.

How to calculate your home equity (fast)

Home Equity Formula

Home Value − Mortgage Balance = Home Equity

Online estimates can be a starting point, but cash-out uses an appraisal or approved valuation method.

Step one is getting a reasonable estimate of your home’s value. For planning, use a conservative value range (low/mid/high), then compare it to your payoff amount.

Example A

$300,000 value

$200,000 owed → $100,000 equity

Example B

$300,000 value

$150,000 owed → $150,000 equity

The rule that controls your cash-out: LTV

LTV stands for loan-to-value. It’s the ratio between your new loan amount and your home’s appraised value. Most cash-out programs cap the maximum LTV—and that cap determines how much cash you can take out.

LTV Formula

Loan Amount ÷ Appraised Value = LTV

Example: If the cap is 80% LTV and your home appraises at $300,000, the max loan is about $240,000 (before program details and closing costs).

Quick planning tip

If your payoff is close to the cap, you may have limited cash-out once closing costs and prepaid items are included.

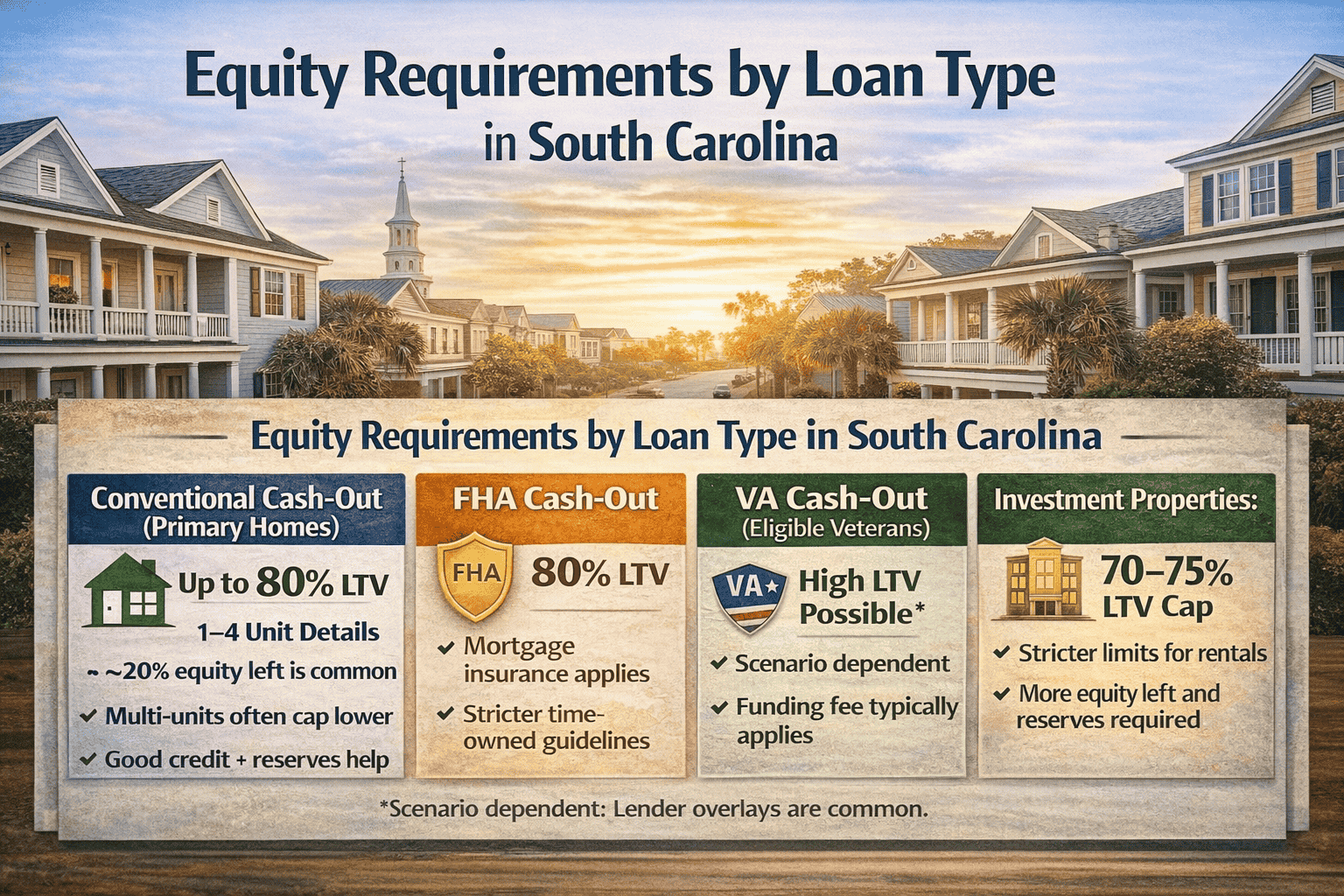

Equity requirements by loan type in South Carolina

Conventional cash-out (primary homes)

- Often capped around ~80% LTV for a 1-unit primary residence

- Multi-unit primary homes may have lower caps (often ~75%)

- Pricing and approval can improve with stronger credit + reserves

FHA cash-out

- Commonly capped around ~80% LTV

- Often requires more time in the home before cash-out eligibility

- Mortgage insurance applies, which impacts the total monthly payment

VA cash-out (eligible veterans)

- Guidelines can allow high LTVs, but lender overlays are common

- Many lenders cap around ~90% LTV (scenario-dependent)

- Funding fee may apply depending on entitlement/usage

Investment properties

- Cash-out is typically more conservative than primary homes

- Common caps are often around ~70–75% LTV depending on program

- Expect stronger documentation and reserve requirements

These are common ranges—not a guarantee.

Your exact cap depends on occupancy, property type, credit profile, lender overlays, and the program you qualify for. If you want the fastest clarity, we can run a scenario and tell you what cap you’re likely on.

South Carolina factors that can change the equity requirement

How much cash can you pull out? (Two quick examples)

For planning, this framework helps (final numbers depend on program rules and closing costs):

Rough cash-out estimate

(Max LTV × Appraised Value) − Current Mortgage Payoff ≈ Cash Available

Planning only — closing costs and prepaid items reduce “cash to you.”

Example 1: 80% cap

Appraised value: $300,000

Max loan @ 80%: $240,000

Current payoff: $200,000

Estimated cash (before costs): $40,000

Example 2: Investment-style cap (75%)

Appraised value: $400,000

Max loan @ 75%: $300,000

Current payoff: $260,000

Estimated cash (before costs): $40,000

Reality check

Closing costs, prepaid items, and program rules can reduce “cash to you.” If you want the real number, the fastest path is a quick scenario review.

Step-by-step: cash-out refinance process in South Carolina

Estimate value + equity

We’ll start with a quick scenario and talk through your goal (debt payoff, renovations, investing, etc.).

Confirm your likely LTV cap

Primary vs investment, 1-unit vs multi-unit, and loan type typically set your limit.

Apply + document income/assets

We’ll collect standard items (paystubs, W-2s, bank statements, leases if applicable).

Appraisal/valuation

The valuation drives the final loan amount and cash-out potential.

Underwriting + conditions

This is where “gotchas” show up—seasoning, property rules, or documentation gaps.

Close + receive funds

Once the refinance closes, funds are disbursed based on the transaction structure.

Cash-out refinance vs HELOC in South Carolina

Cash-out refinance

- One new mortgage

- Typically fixed term + predictable payment structure

- Best when you want a lump sum and clear repayment plan

HELOC

- Line of credit you can draw from over time

- Payment can change as rates/usage change

- Best when you want flexibility (projects over time, emergency access)

If your current first mortgage rate is very low…

It can be worth comparing options carefully—because a cash-out refinance replaces your current loan. We can run both scenarios so you can see the payment difference side-by-side.

FAQs

How soon can you do a cash-out refinance after buying a home in South Carolina?

Many programs require an ownership/seasoning window before cash-out—often measured in months on title and/or time since the first lien note date. The exact rule depends on the program and scenario, and lenders can add overlays. If you share your purchase date and current loan type, we can confirm your earliest likely timeline.

Can you do a cash-out refinance on a manufactured home in SC?

Potentially, yes—if it qualifies as real property and meets program requirements. Manufactured housing guidelines vary by program and property details, so it’s best to review specifics early.

Is a cash-out refinance better than a HELOC?

It depends on your goal. Cash-out is often best for a lump sum with a clear repayment structure. A HELOC can be better for flexibility and phased projects. The right answer usually comes down to your current mortgage rate, how much cash you need, and whether you want fixed vs flexible access.

Final thoughts

A cash-out refinance can be a powerful tool for South Carolina homeowners—when the equity math and the monthly payment both make sense. If you want to move with confidence, focus on the two numbers that matter most: your program’s LTV cap and your all-in monthly payment.

Disclaimer: This content is for educational purposes and doesn’t constitute financial, legal, or tax advice. Program guidelines can change and may vary by lender and borrower scenario.