South Carolina Investor Equity Guide

South Carolina home values have climbed sharply over the last several years—especially in markets like Charleston, Greenville, and Myrtle Beach. If you own a rental or non-owner occupied property, you may be sitting on usable equity you can reinvest.

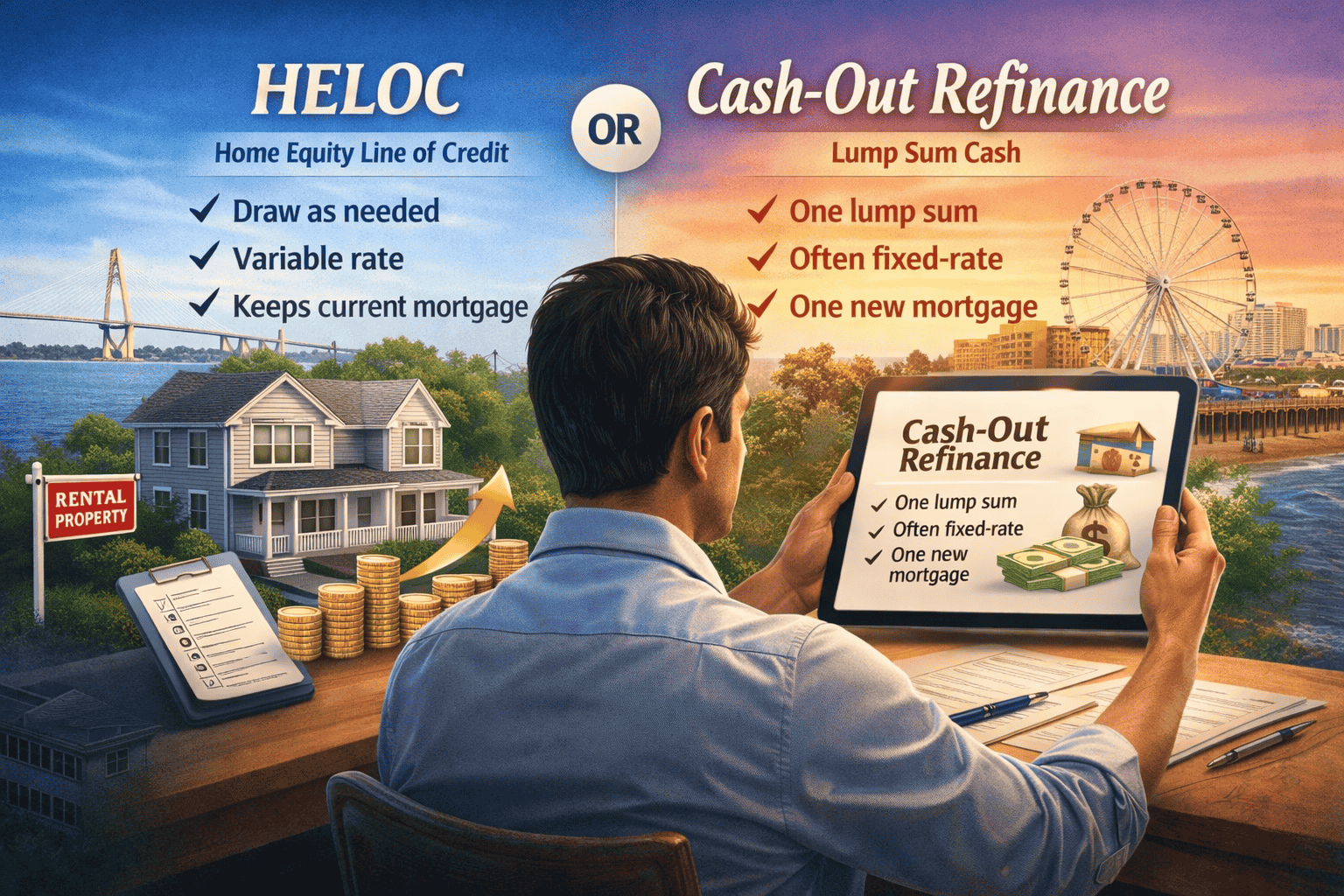

The two most common ways investors tap equity are a HELOC (line of credit) and a cash-out refinance (new mortgage + lump-sum cash). The “best” option depends on your timeline, interest rate comfort, how much cash you need, and whether you’re trying to fund renovations, a down payment, or repeatable buys (BRRRR).

Best for flexibility

HELOC

Borrow as needed (up to limit)

Best for big one-time cash

Cash-out

Lump sum at closing

Common “cap” range

~60–75% LTV

Varies by lender + property

Fast rule of thumb

If you want ongoing access for recurring projects, HELOC usually wins. If you want one large injection of cash and prefer a stable long-term payment, cash-out refinance may fit better.

Quick answer: HELOC vs cash-out refinance for SC investors

Pick a HELOC if you want…

- Flexibility to draw funds as you need them

- Short-term projects, recurring repairs, or multiple small draws

- A tool that pairs well with BRRRR style reinvesting

Best for: ongoing renovations, recurring expenses, multiple properties.

Pick cash-out refinance if you want…

- One large lump sum at closing

- A long-term mortgage structure (often fixed-rate)

- To restructure your existing loan (term, rate, payoff)

Best for: large acquisitions, major rehabs, consolidating strategy into one payment.

Important investor note

On investment properties, equity access is usually more conservative than a primary home. Expect lower max LTV, stronger documentation, and reserve requirements depending on the program/lender.

What is a HELOC for an investment property?

A HELOC (Home Equity Line of Credit) is a revolving credit line secured by your property’s equity. You’re approved up to a limit, and during the draw period (often around 10 years), you can borrow as needed (up to your approved limit).

How a HELOC usually works

- Draw period: borrow and repay (often interest-only payments available).

- Repayment period: payments typically increase because principal repayment begins.

- Rates: commonly variable, so payments can change over time.

Investor tip: HELOCs are popular when you want a reusable “equity engine” for recurring repairs, turns, or smaller acquisitions.

What is a cash-out refinance for an investment property?

A cash-out refinance replaces your current mortgage with a new (larger) loan. The old mortgage is paid off, and you receive the difference as cash at closing (minus closing costs and any required payoffs).

Why investors choose cash-out

Many investors like cash-out when they prefer a clear long-term plan: one payoff, one new mortgage, one structured payment—often with fixed-rate options.

- Best for large one-time needs (big rehab, down payment, acquisition)

- Resets your mortgage term (new amortization schedule)

- Expect 2–5% closing costs in many scenarios

HELOC vs cash-out refinance: quick comparison

Eligibility requirements in South Carolina (what lenders look for)

Equity (what you typically need to keep)

- HELOC: many lenders want you to retain ~15–20% equity.

- Cash-out refi: often more conservative—plan around ~25–30% equity retained.

Exact limits vary by lender, property type, and the strength of the file.

Credit + DTI

- HELOC credit: many lenders prefer ~700+ for investor HELOCs.

- Cash-out credit: many programs start around 680+ (pricing improves with higher scores).

- DTI: many lenders prefer under ~45% (varies by program).

Property type matters (rentals, multi-units, STRs)

HELOCs and cash-out refinance can be available on many property types—single-family, multi-unit, and sometimes short-term rentals. But on investment property, lenders may apply stricter overlays: reserves, lease documentation, appraisal complexity, and occupancy rules.

Heads up

If the property is a short-term rental, you may need stronger income documentation, and local rules (permits/zoning) can impact underwriting.

Pros and cons for investment property owners

HELOC

Pros

- Flexible access to funds when needed

- Interest typically applies only to what you draw

- Great for renovations and repeatable reinvesting

Cons

- Variable rates can increase payments

- Payment changes can complicate budgeting

Cash-out refinance

Pros

- One clear payment structure (often fixed-rate)

- Helps predict long-term costs

- Lump sum can fund major projects or acquisitions

Cons

- Closing costs are usually higher (often 2–5%)

- Mortgage term resets with a new loan

Step-by-step: how to access equity in South Carolina

Estimate your current value

Start with a realistic value range based on recent comps and market activity.

Calculate usable equity

Value − current mortgage payoff = equity (then apply max LTV limits).

Review credit + income docs

Credit score, DTI, and rental income documentation can impact options and pricing.

Compare HELOC vs cash-out scenarios

Same goal, different structure—compare payments, costs, and risk.

Appraisal/valuation + underwriting

Final value and guideline checks determine your final approval and terms.

Close and access funds

HELOC funds become available (up to your limit) or cash-out funds disburse at closing.

FAQs

Can you get a HELOC on an investment property in South Carolina?

Yes. Many lenders offer investor HELOCs, but they often require more equity and stronger credit than a primary home.

Is a cash-out refinance harder on an investment property?

Usually, yes. Investment-property cash-out typically requires more equity, stricter LTV limits, and stronger documentation than owner-occupied.

Which is cheaper: HELOC or cash-out refinance?

It depends on current rates, how long you’ll carry the balance, and closing costs. HELOCs can be cheaper for short-term use; cash-out may win if you need long-term stability.

Can short-term rentals qualify in South Carolina?

Often yes, but documentation and property rules can be stricter. You may need stronger income documentation, and local ordinances can matter.

Bottom line

If you’re trying to tap equity on an investment property in South Carolina, both HELOC and cash-out refinance can work— but they solve different problems. The right move comes down to how much cash you need, how long you need it, and how comfortable you are with variable rates vs a structured mortgage payment.

Disclaimer: This content is for educational purposes and doesn’t constitute financial, legal, or tax advice. Program guidelines can change and may vary by lender and borrower scenario.