South Carolina Investor Loan Guide

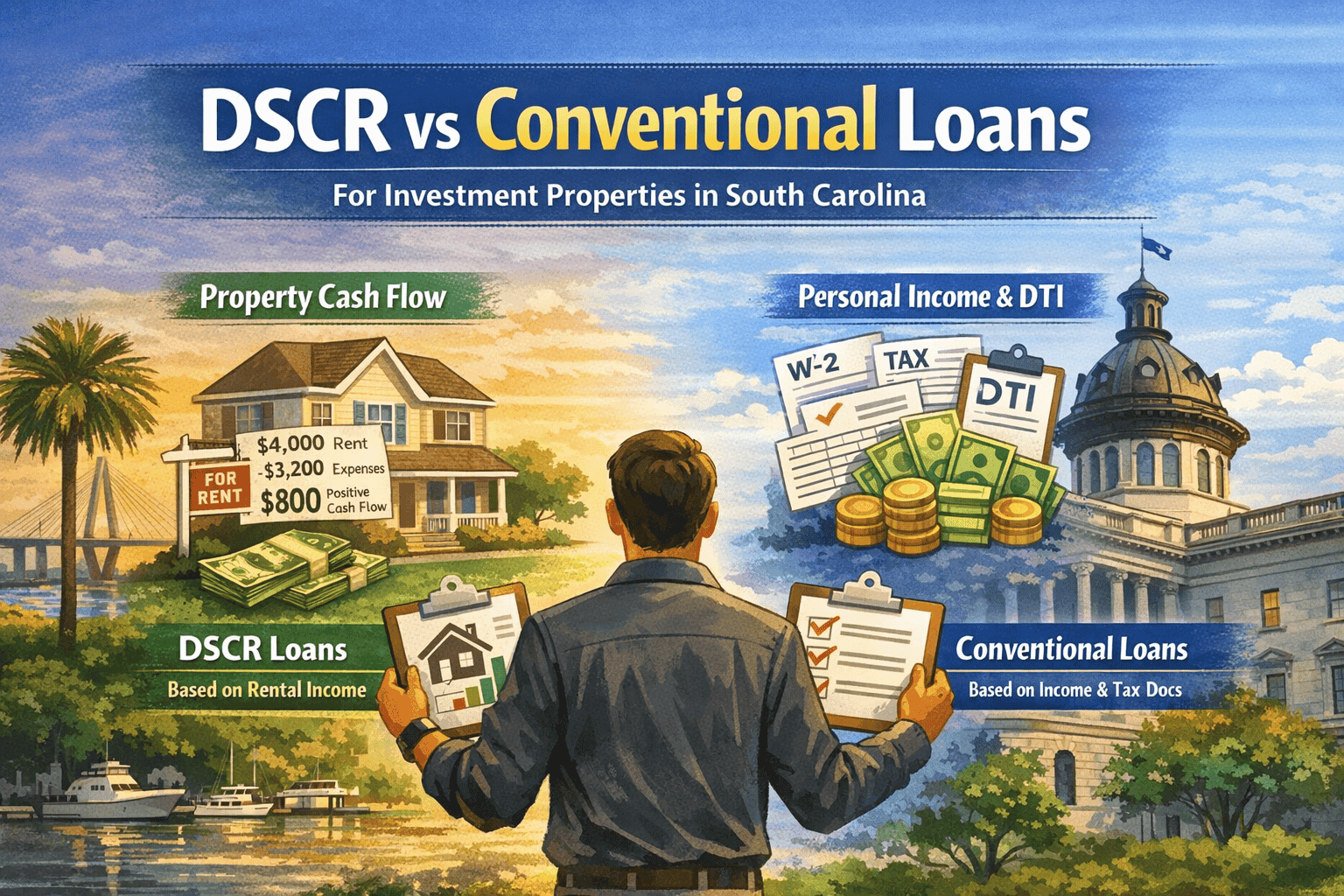

DSCR loans and conventional investment property loans can both work in South Carolina—but they qualify you in totally different ways. DSCR focuses on the property’s rental income and cash flow, while conventional focuses on your personal income, debt, and documentation.

If you’re investing in places like Greenville, Charleston, Columbia, Myrtle Beach, Spartanburg (or anywhere in between), the right choice impacts your cash flow, how fast you can scale, and what kind of returns you lock in long-term.

DSCR qualifies with

Rental Cash Flow

Not your DTI

Conventional qualifies with

Personal Income

Full docs + DTI

Best “first step”

Run DSCR

Before you apply

Fast rule of thumb

If you want to grow a portfolio without getting boxed in by personal debt-to-income limits, DSCR is usually the cleaner path—especially for self-employed investors or anyone with multiple properties.

A quick overview of DSCR vs conventional loans

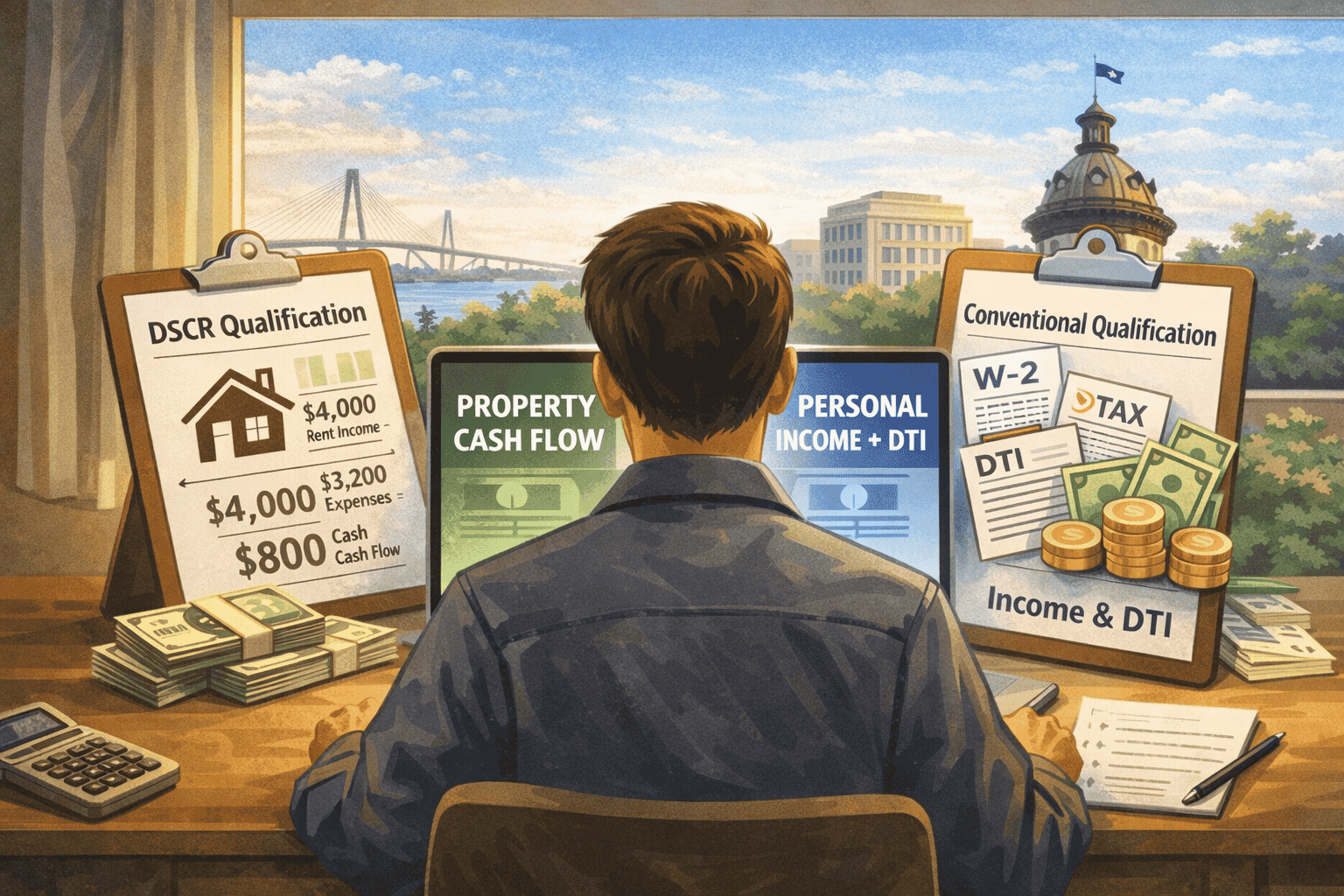

Here’s the simple breakdown: DSCR loans qualify the property. Conventional loans qualify you.

DSCR loans

Built for investors. Approval is based on whether rental income can cover the mortgage payment. Often no tax returns and no DTI-based qualifying in many scenarios.

Conventional investment loans

Often tied to Fannie/Freddie-style guidelines. Approval is based on personal income, DTI, and documentation. Can offer lower rates if you qualify strongly.

What is a DSCR loan?

A DSCR loan checks whether your investment property generates enough rent to cover its own mortgage payment. DSCR stands for Debt Service Coverage Ratio.

Simple DSCR concept

DSCR = Monthly Rent ÷ Monthly Housing Payment

Housing payment often includes PITI (and sometimes HOA, depending on program)

Why investors like DSCR

It’s built for scaling: qualification is centered on the property, not your personal DTI. In many scenarios, you can avoid tax returns and paystubs.

What is a conventional investment property loan?

A conventional investment property loan is a more traditional mortgage option—often aligned with Fannie Mae / Freddie Mac style rules—where approval is based on your personal income, DTI, and documentation.

What to expect

Conventional financing usually means more paperwork: tax returns, W-2s, paystubs, bank statements, and a deeper review of your personal debts and obligations.

Key qualification differences (what actually changes)

Income requirements

DSCR: property-focused. Lenders want the property to support the payment.

Conventional: personal income-focused with full documentation (often 2 years).

Down payment & LTV

DSCR: commonly 20%–30% down (scenario dependent).

Conventional: often 15%–25% down depending on property and profile.

Credit score expectations

DSCR: many scenarios start around 620–680+.

Conventional: often 640–700+ for the strongest pricing.

Portfolio scaling

DSCR: designed for investor portfolios and scaling strategies.

Conventional: may tighten as financed property count rises (often around ~10).

Interest rates, costs, and the cash flow impact

Conventional loans can offer lower rates if your income, DTI, and documentation are strong. DSCR rates can run higher because the loan is underwritten as an investment product—but the structure can keep your cash flow healthier (especially when conventional would limit your borrowing due to personal DTI).

Typical closing costs

~2%–5%

Scenario dependent

DSCR advantage

Scaling

Property-driven approval

Conventional advantage

Rate

If you qualify strongly

Best next step

If cash flow is your main concern, run DSCR first: Rental Property (DSCR) Calculator.

Property types & usage in South Carolina

DSCR is often a strong fit for long-term rentals—and can also work for short-term rentals depending on the program rules. Conventional can work well for basic rentals, but may be less flexible for STR scenarios and portfolio growth.

Local investor notes

- Charleston: tourism demand can support STR strategies—but underwriting may be conservative.

- Greenville: strong demand for family homes, workforce rentals, and small multifamily.

- Columbia: price points often make it easier to stack properties and scale.

- Myrtle Beach: seasonal income patterns matter—document the rent story cleanly.

Which loan is better for South Carolina investors?

The best option depends on how you earn income, how many properties you plan to finance, and whether your strategy is focused on cash flow or rate optimization.

Go DSCR when:

- You’re self-employed or don’t want heavy income documentation

- You’re scaling beyond a few properties and want less DTI friction

- Cash flow from the property is the primary decision-maker

- You want a cleaner, property-first qualification path

Go conventional when:

- You have strong W-2 income and low personal debt

- You want the lowest possible rate on 1–2 rentals

- You can handle full documentation and DTI requirements

- You plan long holds and want to remove PMI later (when applicable)

Quick example

If a Charleston duplex rents for $2,500/month and the full housing payment is $1,900/month, the DSCR is about 1.32—often a strong ratio for DSCR financing.

Loan approval & timeline comparison

DSCR underwriting is usually more straightforward—appraisal, rent/lease documentation, and a property-first review. Conventional can take longer because income documentation and DTI analysis are heavier.

DSCR timeline

Often 21–35 days with a clean file.

Common docs: leases, appraisal, bank statements (scenario dependent).

Conventional timeline

Often 30–45 days due to documentation.

Common docs: paystubs, W-2s, tax returns, full DTI review.

Quick comparison table

| Aspect | DSCR Loans | Conventional Loans |

|---|---|---|

| Key Documents | Leases/rent evidence, appraisal (often no tax returns) | Pay stubs, W-2s, tax returns, deep income verification |

| Underwriting | Property-focused cash flow review | Personal income + DTI focused |

| Typical Timeline | 21–35 days | 30–45 days |

| Scaling | Investor-friendly for portfolios | Often tightens as property count grows |

If you only do one thing today…

Use the DSCR Calculator to see whether the property supports the payment. That one number will usually tell you which direction makes more sense.

Frequently asked questions

Is a DSCR loan better than a conventional loan for investors?

It depends on your income setup and your growth goals. DSCR is often better for scaling and for self-employed investors because approval is based on rental cash flow instead of personal DTI.

Can I use a DSCR loan for short-term rentals in South Carolina?

Often yes—depending on program rules and how income is documented. Some scenarios use market rent, while others consider rental history or third-party STR reports.

Do conventional loans usually have lower interest rates?

Usually, yes—if you have strong credit, solid income, and clean documentation. DSCR pricing can be higher, but it may still be the better tool if conventional DTI limits would restrict your portfolio growth.

How many investment properties can I finance with each loan type?

Conventional financing often tightens as financed property count increases (commonly around ~10). DSCR is typically more portfolio-friendly, though program limits can still apply.

Which loan is easier to qualify for?

Many investors find DSCR easier because it avoids heavy income documentation and focuses on the property’s ability to cover the payment.

Bottom line

DSCR loans give South Carolina investors flexibility by qualifying based on rental income—great for scaling portfolios without getting boxed in by personal DTI and heavy documentation. Conventional loans can be a strong fit when you have clean W-2 income and want the lowest possible rate on a small number of rentals.

Want the fastest clarity? We’ll run the numbers and tell you which path makes sense for your property and goals.

Disclaimer: This content is for educational purposes and doesn’t constitute financial, legal, or tax advice. Program guidelines and pricing can change and vary by scenario.