Investor Loan Guide

A DSCR loan (Debt-Service Coverage Ratio loan) is an investor-friendly mortgage that focuses more on the property’s rental income than your personal income. If you’re buying or refinancing a rental, DSCR can be a cleaner path to financing — especially when you want to scale beyond one or two properties.

Income-based approval

Qualify based on rent vs. payment — not W2s alone.

Scale faster

Often easier to repeat than conventional investor loans.

Use cases

Purchase, refi, cash-out refi (program dependent).

DSCR loan basics (what it is — and what it isn’t)

DSCR stands for Debt-Service Coverage Ratio. In plain terms, it measures whether a rental property’s income can cover its monthly debt obligation. A DSCR loan uses that ratio as a major qualifying factor, which is why it’s popular with investors.

Fast definition

A DSCR loan is a mortgage for rental properties where approval is driven primarily by the property’s rental income compared to the mortgage payment (and sometimes other housing costs), rather than your personal debt-to-income ratio alone.

When DSCR loans make the most sense

- Buying a long-term rental (single-family, 2–4 unit, or other eligible property types)

- Refinancing to improve rate/term or pull equity (program dependent)

- Growing a rental portfolio where W2 income doesn’t tell the full story

- Self-employed investors who want a simpler documentation path

What DSCR loans are not

- They’re not the same as hard money (DSCR is typically long-term rental financing).

- They’re not “no underwriting.” Credit, reserves, appraisal, and property analysis still matter.

- They’re not automatically the cheapest option — they’re often chosen for flexibility + scalability.

Want to see your DSCR quickly?

Use our Rental Property (DSCR) Calculator to estimate payment, expenses, and DSCR in minutes.

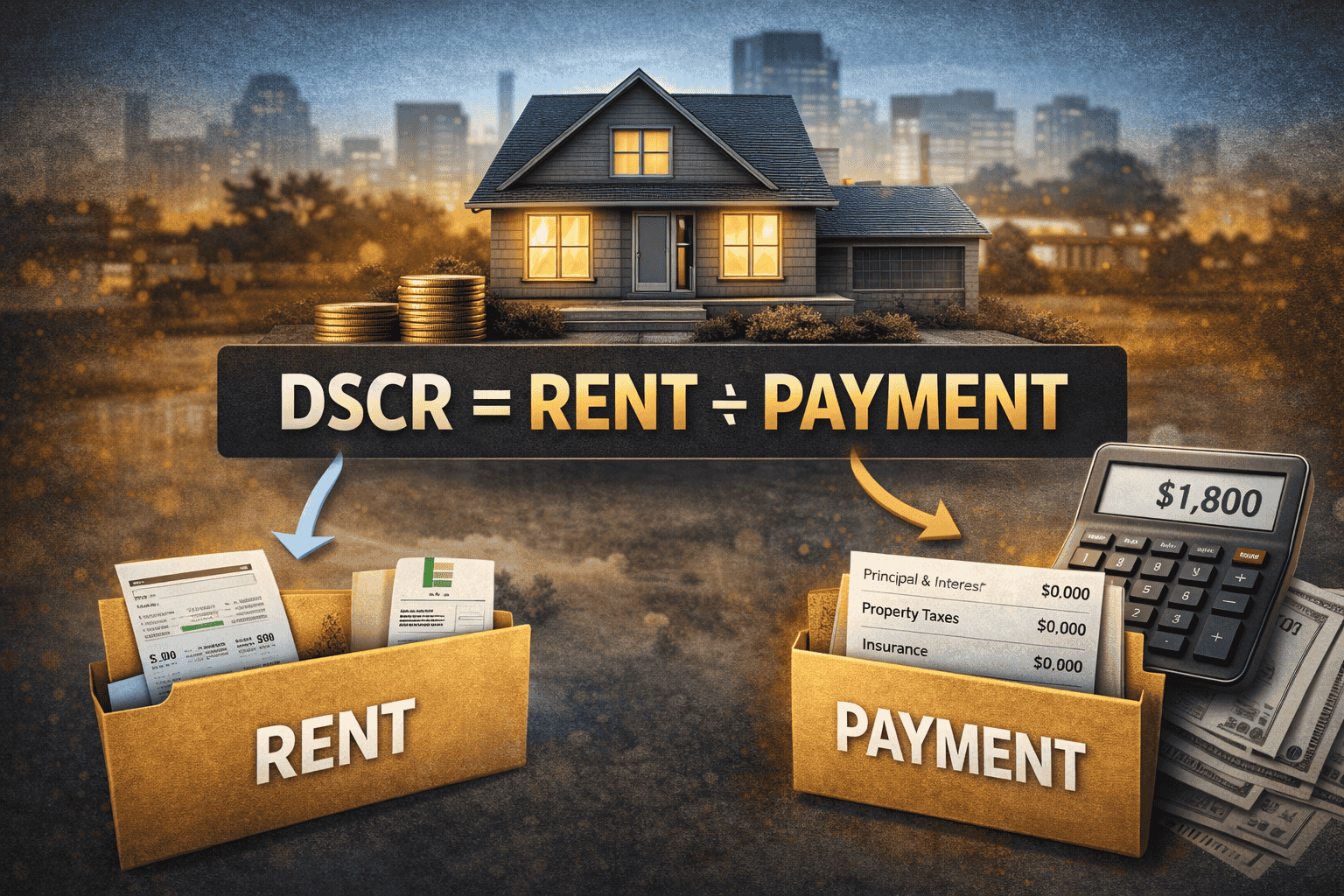

How DSCR is calculated (the ratio that drives approval)

DSCR is a ratio. Ratios are simple: the top number is what the property brings in, and the bottom number is what the property costs you in monthly debt payment (and sometimes housing costs).

Common DSCR formula

DSCR = Gross Monthly Rent Monthly Debt Payment

“Monthly debt payment” is typically principal + interest, and often includes taxes + insurance depending on the program/lender.

What counts as “rent”?

Most lenders use either the lease amount (if there’s a valid lease) or the appraiser’s market rent estimate (often from a rent schedule). Some lenders may use a percentage of market rent or apply conservative adjustments.

What’s a “good” DSCR?

- 1.00 = rent equals the payment (break-even)

- 1.10–1.25 = healthier buffer (common target ranges)

- 1.30+ = strong coverage (often improves pricing/approval options)

Important note

DSCR requirements vary by lender, property type, and scenario (purchase vs. refi). A deal that’s “close” can often be improved with structure — like adjusting down payment, expenses, or insurance assumptions.

DSCR example (simple math you can do on the back of a napkin)

Scenario

- Gross Monthly Rent: $2,200

- Monthly Payment (P&I + escrows): $1,850

Calculation

2,200 ÷ 1,850 = 1.19 DSCR

This deal has a cushion — the property generates about 19% more rent than the monthly debt payment.

How to improve DSCR (if you’re under the threshold)

- Increase down payment to lower loan amount and payment

- Verify market rent with strong comps (supporting appraiser value/rent)

- Shop insurance realistically (overestimated insurance can hurt DSCR)

- Lower the rate via structure (points / lender options / timing)

- Choose the right product (different DSCR programs can underwrite differently)

Run the numbers in 2 minutes

Estimate payment + DSCR using your rent and expenses.

How investors qualify (what lenders actually look at)

Even though DSCR emphasizes the property’s income, lenders still evaluate risk. Here are the main buckets that usually determine approval and pricing:

1) The property

- Appraised value and marketability

- Market rent (rent schedule / lease)

- Condition (habitability, required repairs)

- Taxes + insurance assumptions

2) The borrower

- Credit profile (score, history, major derog)

- Liquidity / reserves (cash on hand after close)

- Experience (helps in some scenarios, not always required)

- Entity setup (LLC/vesting rules vary by program)

Purchase vs. refinance

DSCR is often used for both purchases and refinances. The main difference is how value, rent, and loan amount are underwritten. Refinances may also consider seasoning, payoff statements, and how you’re pulling equity (if any).

Quick reminder

If you’re comparing DSCR to other options, check out: Cash-Out Refinance vs HELOC (use-case differences matter when you’re optimizing cash flow).

Documents you’ll typically need (to keep underwriting moving)

Every lender is slightly different, but you can usually speed things up by having these ready early:

- Purchase contract or payoff statement — contract for purchases; payoff + mortgage statement(s) for refinances.

- Lease agreement (if occupied) — current lease helps support rent; if vacant, rely on market rent analysis.

- Insurance quote — accurate insurance matters; overestimates can hurt DSCR.

- Entity docs (if vesting in an LLC) — articles/operating agreement, EIN letter, and authorization as required.

- Bank statements / reserves proof — most programs want to see cash reserves after closing.

Want a fast pre-check?

Send the address, estimated rent, and purchase price — we’ll tell you if it’s in range.

Pros & cons of DSCR loans (so you choose the right tool)

Why investors like DSCR

- Less reliance on personal income than traditional DTI-based underwriting

- Repeatable process as you acquire more rentals

- Works well for self-employed investors (program dependent)

- Often compatible with LLC vesting (rules vary)

Tradeoffs to consider

- Pricing can be higher than conventional options

- Reserves may be required (cash on hand after closing)

- Low-rent markets can struggle to meet DSCR

- Insurance/taxes assumptions can shift the ratio

If your priority is the lowest possible rate and you have strong personal income/DTI, a conventional investor loan may still win. If your priority is scaling and cleaner rental-based qualification, DSCR is often the better fit.

Common DSCR mistakes (and how to avoid them)

- Using optimistic rent numbers. If the appraiser can’t support it, your DSCR can drop. Use realistic comps and leases.

- Ignoring insurance impact. High insurance quotes can crush DSCR. Get a real quote early and update the structure.

- Forgetting about reserves. Even with good DSCR, low liquidity can slow or stop approval. Plan cash to close + reserves.

- Waiting to share entity docs. If you’re buying in an LLC, send docs up front so vesting doesn’t become a last-minute issue.

Pro move

Run your deal through the DSCR Calculator before you submit — and build a cushion for insurance/taxes. It’s the easiest way to avoid underwriting surprises.

Next steps (a simple path to get a DSCR loan)

1

Run the DSCR

Estimate payment, taxes/insurance, and DSCR so you know where you stand.

2

Confirm rent support

Lease or market rent comps — keep the appraisal aligned with reality.

3

Choose the structure

Down payment, rate options, reserves, and entity vesting (if applicable).

4

Submit + move

Upload docs quickly so underwriting can clear conditions and close clean.

DSCR loan FAQs

What does DSCR stand for?

DSCR stands for Debt-Service Coverage Ratio. It compares a property’s rental income to its monthly debt payment to measure cash flow strength.

What DSCR do I need to qualify?

It depends on the lender and scenario. Many programs look for around 1.00+, while stronger ratios (like 1.10–1.25+) can improve approval and options.

Do DSCR loans require tax returns?

Some DSCR programs reduce reliance on personal income documentation, but requirements vary. Lenders still review credit, assets, the property, and rent support.

Can I close a DSCR loan in an LLC?

Often yes, depending on program guidelines. If you’re vesting in an entity, plan to provide entity documents early to avoid last-minute delays.

Is a DSCR loan good for first-time investors?

It can be. Many first-time investors use DSCR successfully, especially when the rent supports the payment and they have a realistic budget for reserves and repairs.

What’s the biggest reason DSCR loans get denied?

Most issues come down to rent support, property condition, or liquidity/reserves. Running the numbers early and documenting rent assumptions helps a lot.

Can I use projected rent on a vacant property?

Typically, lenders rely on an appraiser’s market rent estimate (rent schedule) when there’s no lease. They may apply conservative adjustments depending on guidelines.

How do I quickly estimate my DSCR before applying?

Use our Rental Property (DSCR) Calculator to estimate principal & interest, taxes, insurance, expenses, and DSCR in minutes.

Disclosure: Examples are for educational purposes only. Actual terms, DSCR requirements, and program availability vary by borrower profile, property details, and market guidelines.