Fix & Flip Funding

Funding your first fix & flip isn’t just “getting a loan” — it’s building a plan that matches your timeline, budget, and exit strategy. This guide breaks down the numbers lenders care about, the funding options investors actually use, and the step-by-step process to get a deal from offer to closing.

If you want faster approvals, smoother draws, and fewer surprises, the goal is simple: present a clean deal package and run your numbers before you submit.

Fix & flip funding basics

Most first flips have three phases: buy, renovate, and sell. Your financing plan needs to support all three — without draining your cash reserves.

Quick reality check: time is a cost. Every extra week adds holding expenses and can reduce profit. A “great deal” can turn average if the timeline gets away from you.

What fix & flip financing typically includes

- Short-term loan built for renovations (often 6–12 months).

- Purchase + rehab structure (varies by lender and deal strength).

- Interest-only payments are common, with payoff at sale or refinance.

- Rehab funds released in stages (draws) as work is completed.

Funding options investors use for a first flip

Fix & Flip Loan (Hard Money)

Built for speed. These loans focus heavily on the deal, the scope, and the exit strategy — and they’re commonly paired with rehab draws.

- Fast approvals and closings

- Designed for renovations

- Short-term payoff at sale or refinance

Cash / Private Capital

Cash can make offers stronger, but it can also overexpose you if repairs run long or the market shifts. If you use private capital, define terms clearly (timeline + exit).

- Less friction, fewer steps

- Potentially higher risk concentration

- Get agreements in writing

HELOC / Home Equity

Some investors use equity to cover down payments, reserves, or repair gaps. It can be a smart tool — but it also ties your primary residence to the project.

- Can supplement a flip loan

- Often flexible access

- Higher personal risk if overused

Bridge Plan + Backup Exit

If you’d consider holding the property as a rental if the market changes, plan for it up front. A strong deal has a primary exit and a backup exit.

- Plan A: Sell for profit

- Plan B: Refinance/hold

- Protects you if timelines shift

Pro move: choose funding that matches your timeline and reserves — not just the “lowest rate.” Cheap money isn’t cheap if it slows your project down.

Lender-ready deal package checklist

If you want fast underwriting decisions, submit a clean deal package. This is the same structure experienced investors use to keep approvals and draw requests moving.

- Property address + purchase contract (or HUD/settlement statement if already owned)

- After-Repair Value (ARV) estimate supported by comps

- Scope of work (room-by-room) + line-item rehab budget

- Timeline (start date, milestone phases, estimated completion)

- Exit strategy: sell, or refinance/hold as a backup plan

- Borrower details: ID + entity docs (if applicable)

- Liquidity/reserves: recent bank statements

- Contractor info (if required): bid, license/insurance where applicable

Want help packaging it? Run your deal through the calculator, then submit when ready.

What fix & flip lenders look for

The deal

Purchase price, ARV, rehab scope, and whether there’s enough margin to handle risk.

The plan

A realistic timeline, a clean scope of work, and a clear exit strategy (sell or refinance).

The borrower

Liquidity/reserves, credit profile, and how prepared you are to execute.

The property

Neighborhood comps, demand, and whether your rehab aligns with what buyers pay for.

First flip tip: you don’t need to “prove you’re a pro.” You need to show the numbers are clean and your plan is realistic.

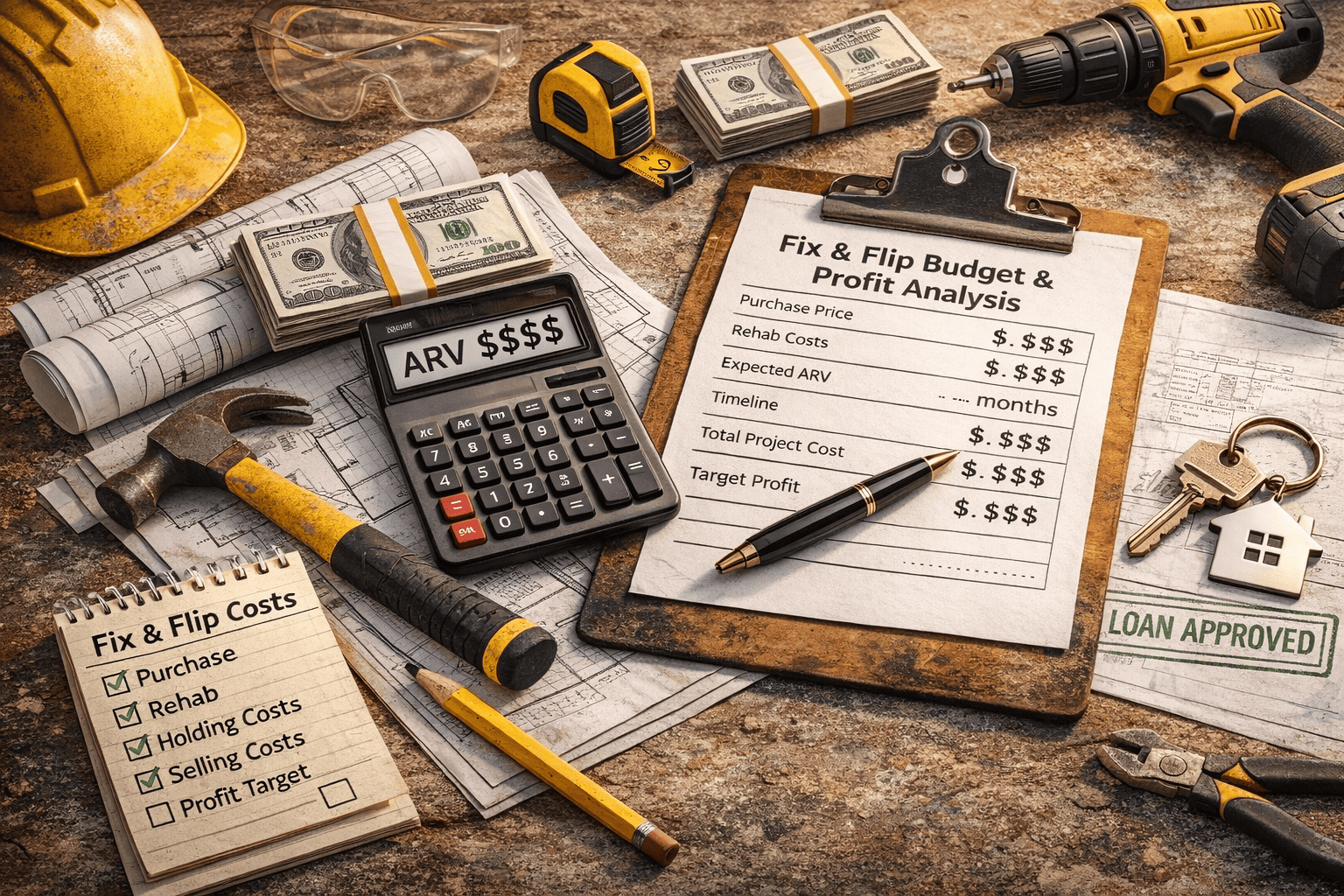

The 5 numbers you must know before you fund a flip

1

Purchase Price

What you’re paying today — and whether you’re buying it right.

2

Rehab Budget

Line-item renovation costs plus a contingency buffer.

3

After-Repair Value (ARV)

Expected value after renovations — supported by comps.

4

Timeline

Rehab duration plus listing time — delays cost money.

5

Total Project Cost

Purchase + rehab + holding + selling costs = real profit clarity.

Quick math: If your timeline slips by 30–60 days, your holding costs and interest can eat into profit fast. Build your budget around a realistic schedule — not a “best case” schedule.

Want a quick profit estimate?

Use our Fix & Flip Calculator to map your purchase, rehab, and projected profit.

Build a flip budget that holds up under pressure

The fastest way to stall a project is underestimating budget or forgetting “non-renovation” costs. Your scope and budget should be detailed enough that a lender (and your contractor) can follow it without guesswork.

Scope of work should include

- Room-by-room tasks

- Material/finish level (basic, mid, high)

- Labor estimates + who’s doing what

- Start + completion targets

Costs first-time flippers miss

- Dumpster / hauling

- Permits / inspections

- Utilities during rehab

- Landscaping & curb appeal

- Contingency reserve

Don’t skip contingency: renovations are unpredictable. A buffer protects your timeline and your profit.

Don’t forget holding & selling costs

- Holding costs: interest, taxes, insurance, utilities, HOA (if applicable).

- Selling costs: agent commission, closing costs, seller concessions.

- Financing costs: points and fees depending on structure.

Draws, inspections, and timelines

Many fix & flip loans release rehab funds in stages called draws. The goal is simple: keep the project moving and match funding to completed work.

1

Complete a phase of work

Work should match your scope (example: demo + framing, or flooring + paint).

2

Request a draw

Submit photos, invoices, or the draw form based on the lender’s process.

3

Inspection / verification

Work is verified against the scope before funds are released.

4

Funds released

Rehab funds are released so you can start the next phase.

Speed tip: keep your scope organized, document progress with photos, and communicate early when change-orders come up.

Step-by-step: how to get funded for your first fix & flip

- Find a deal with margin. Back ARV with comps and leave room for surprises.

- Build a clear scope of work. Line items, materials, and a timeline.

- Estimate total project cost. Rehab + holding + selling costs.

- Prepare your docs. ID, entity docs (if applicable), and bank statements.

- Submit the deal package. Clean info = faster decisions.

- Close and execute. Stay organized so draws run smoothly.

- Exit with confidence. Sell — or pivot to refinance/hold if the numbers support it.

Fix & flip funding FAQs

Can I get a fix & flip loan for my first flip?

Yes. First-time investors can still get funded. Strong preparation (numbers, scope, and realistic timeline) matters a lot.

What does ARV mean?

ARV is the after-repair value — the estimated value once renovations are complete. It should be supported by comparable sales.

What are rehab draws?

Draws are staged releases of rehab funds after work is completed and verified. They help align funding with progress.

What documents should I have ready?

At minimum: photo ID, entity docs (if applicable), recent bank statements, and a clear deal package (purchase, rehab, ARV, timeline).

What if I decide to keep it as a rental instead of selling?

That’s why exits matter. If the numbers support it, refinancing into longer-term financing may be an option after renovations are complete.

Want a second set of eyes on your deal? If you’re not ready to apply yet, you can still reach out with questions anytime. Contact us here →