Refinance Guide (No Cash-Out)

We talk with homeowners every day who ask the same thing: “Is refinancing worth it if I’m not walking away with cash?” In many cases, yes — because the win isn’t a payout. It’s lower monthly cost, better terms, and a loan that fits your life long-term.

This is called a rate-and-term refinance (also known as a no cash-out refinance): you replace your current mortgage with a new one primarily to improve your rate, term, or structure — without tapping equity for a lump sum.

Best reason

Lower cost

Rate and interest savings

Big decision point

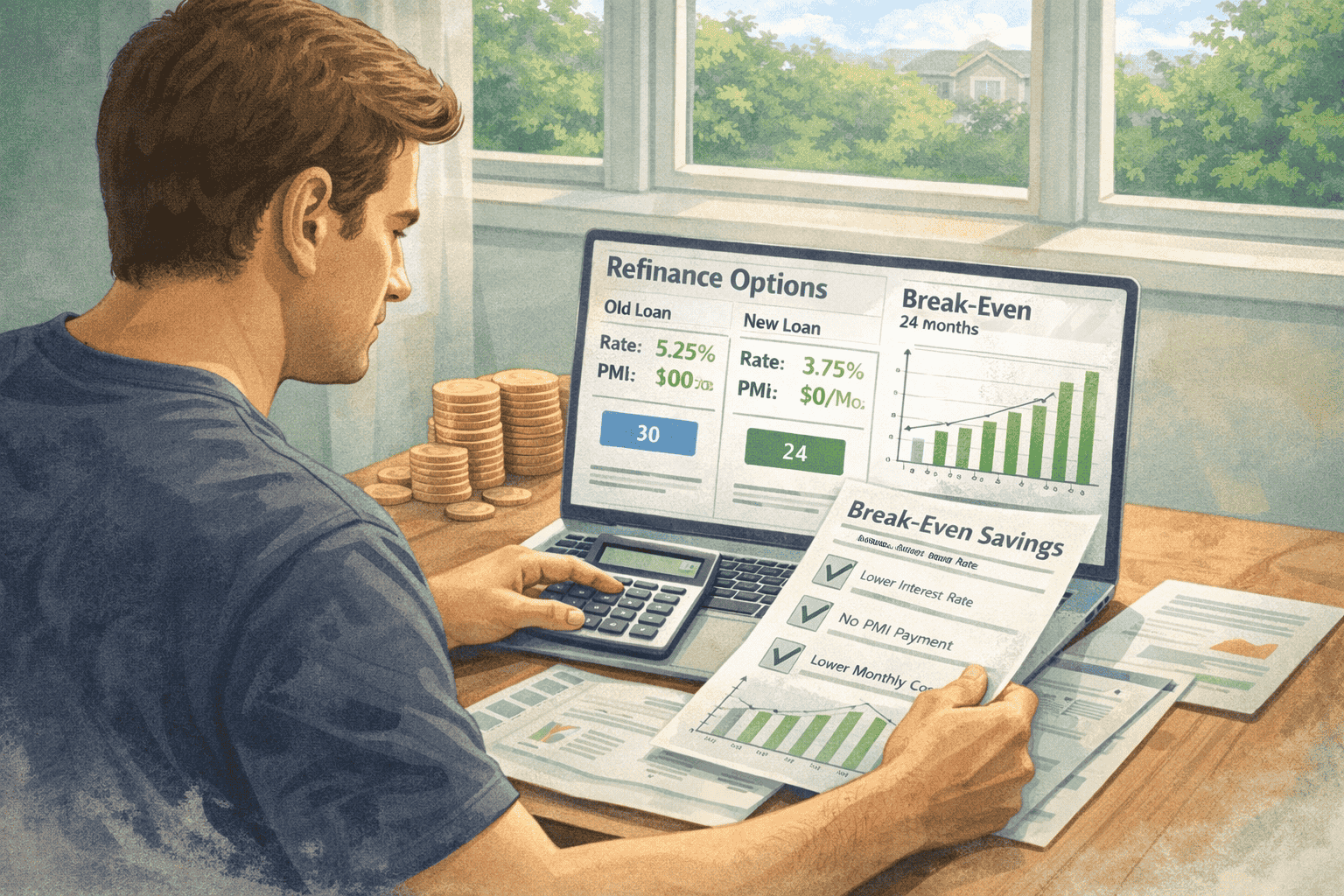

Break-even

When savings beat costs

Hidden win

Remove PMI

If equity supports it

Fast rule of thumb

If your new rate + terms save enough to recoup closing costs within a reasonable window (often 24–36 months), a no cash-out refinance can be a smart move. The key is running the numbers — not guessing.

What is a no cash-out (rate-and-term) refinance?

A no cash-out refinance is like hitting reset on your mortgage with better settings. You take out a new loan that pays off your existing mortgage — but the new balance is typically close to what you currently owe (plus closing costs if they’re rolled in).

What changes

Rate, term length, loan type, or mortgage insurance.

What doesn’t

You’re not taking a lump sum out of your equity for cash.

Important clarification

If you receive a meaningful amount of cash back at closing (beyond small adjustments), that can shift this into cash-out refinance territory depending on the program.

Common reasons homeowners refinance without cash out

If you’re not getting cash, you’re usually getting peace of mind — and a payment structure that fits your goals. Here are the most common wins we see.

Top reasons people choose rate-and-term refinance

- Lower your interest rate: even a modest drop can save thousands over the life of the loan.

- Reduce monthly payments: free up cash flow for life, repairs, savings, or investing.

- Shorten the loan term: go from 30-year to 15-year to pay far less interest overall.

- Switch loan type: FHA → conventional (potentially remove lifetime MIP), ARM → fixed, or use VA IRRRL.

- Remove PMI: if equity and guidelines support it, refinancing can eliminate PMI.

When refinancing does not make sense

Refinancing is a tool — not a rule. It may not be worth it if the math doesn’t support the move.

- Closing costs are too high: if fees outweigh savings, it’s not a win.

- You’ll sell soon: if you move before break-even, you may never recoup costs.

- Your credit has dropped: pricing may not improve enough to justify the reset.

- Loan balance is small: savings may be minimal compared to costs.

Quick reality check

The goal isn’t “refinance because rates moved.” The goal is refinance because your total cost improves.

Key financial factors to evaluate before you refinance

Before you sign anything, pressure-test the numbers using these three pillars.

1) Break-even point

Divide your total closing costs by your monthly payment savings. That tells you how many months it takes to “earn back” the refi.

Example: $4,000 costs ÷ $150/mo savings ≈ 27 months to break even.

2) Credit + pricing

Better credit can improve pricing, especially when you’re near key score tiers. Many conventional programs look for ~620+, but higher scores can improve options.

3) Home value + equity (location matters)

Home value impacts your loan-to-value and eligibility. If your property is in a strong market, improved value can unlock better terms, lower MI, or PMI removal (scenario dependent).

How the no cash-out refinance process works

If the savings are real, the process is usually straightforward — and often faster than a purchase.

- 1Review your current loan. Rate, balance, term, and mortgage insurance.

- 2Compare today’s rates. Focus on total monthly payment and lifetime interest.

- 3Apply + submit documents. Income, assets, and property info.

- 4Appraisal (if required). Confirms value and supports pricing/MI decisions.

- 5Close. New loan pays off the old loan — improved terms begin.

Frequently asked questions

Is refinancing worth it without taking cash out?

Yes — when it lowers your interest rate, reduces payment, or lowers total interest over the life of the loan.

How much does refinancing typically cost?

Closing costs are often around 2%–5% of the loan amount, depending on program, property, and third-party fees.

How much should rates drop to refinance?

Many refinance when rates drop 0.5%–1%, but the real answer depends on loan balance, costs, and how long you’ll keep the home.

Can I refinance just to remove PMI?

Often, yes — if your value/equity supports it and you qualify for a conventional loan structure that doesn’t require PMI.

How long should I stay in my home after refinancing?

Usually at least 2–3 years, but the best benchmark is your break-even month. Stay past break-even to come out ahead.

Bottom line

A no cash-out refinance isn’t about getting money back — it’s about improving the structure of your mortgage. If the break-even timeline is reasonable and the total cost goes down, it can be one of the cleanest ways to strengthen your long-term finances.

If you want clarity fast, run the numbers — and we’ll sanity-check the result with you.

Disclaimer: This content is for educational purposes and doesn’t constitute financial, legal, or tax advice. Program guidelines and pricing can change and vary by scenario.