Start smart. Shop confidently. Close faster.

Before you fall in love with a home—or start running numbers on your next investment—it helps to know what you can comfortably qualify for. A mortgage pre-approval gives you clear buying power, stronger offers, and fewer surprises later—whether you’re purchasing, refinancing, or financing an investment property.

What Is Mortgage Pre-Approval?

Mortgage pre-approval is a lender’s way of saying: “Based on what we’ve reviewed, you qualify up to a certain amount.” It means your income, credit, and assets have been evaluated so you can shop with confidence—often with an estimated rate and a loan path that fits.

Think of it like this:

A pre-approval isn’t just a piece of paper. It’s your home-shopping power tool—and it helps you move faster when the right property shows up.

Pre-Approval vs. Prequalification: What’s the Difference?

Prequalification

- Quick estimate based on basic info you provide

- Typically no document review

- Usually no credit pull

- Helpful for early planning

Pre-Approval

- Deeper review of your financial picture

- Document verification + credit review

- More accurate numbers

- Sellers take it seriously

Want to run quick numbers first? Try the Mortgage Calculator or the DSCR Rental Calculator if you’re buying a rental.

Why Pre-Approval Matters

Getting pre-approved sets the tone for your entire homebuying or investment journey. Here’s why it’s worth it:

- You’ll know your budget (no more guessing).

- Sellers take your offer seriously—especially in competitive markets.

- You uncover issues early (credit, documentation, debt-to-income).

- You can move faster when the right property shows up.

Ready to make this real?

A quick application gets you accurate numbers so you can shop confidently.

Buying, Refinancing, or BRRRRing? Pre-Approval Covers It All

We provide pre-approvals across multiple loan types, including:

Home Loans (FHA, VA, Conventional)

Great for first-time buyers, move-up buyers, and traditional home purchases or refinances.

DSCR Loans

For investors qualifying with rental income. Run numbers with the DSCR Rental Calculator.

Fix & Flip Loans

Move fast when deals pop up. Estimate profit with the Fix & Flip Calculator.

Refinance Options

Lower your rate or cash out equity—get clarity using the Refinance Calculator.

HELOCs

Access home equity with a flexible line of credit. Start with the Home Equity Calculator.

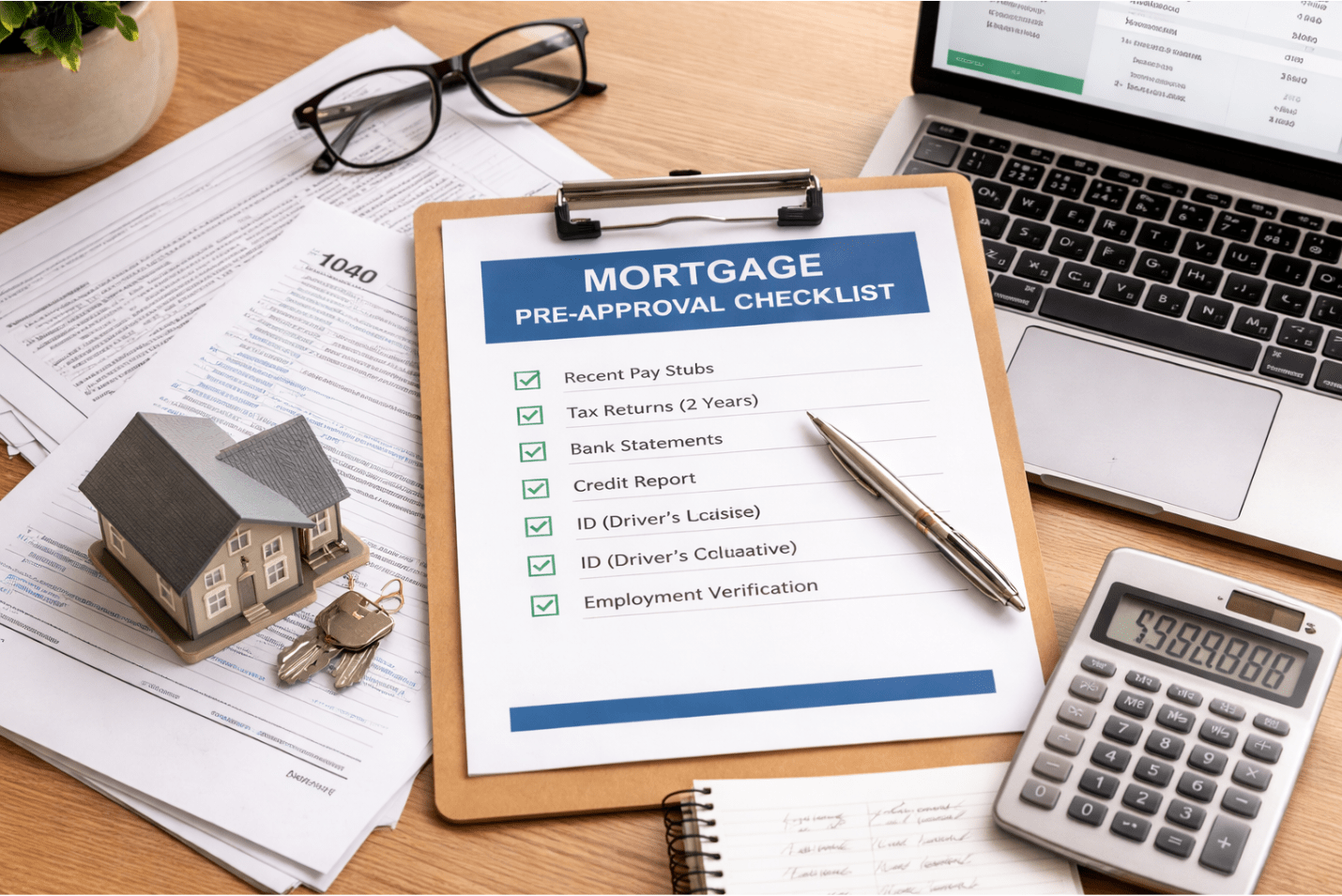

What You Need To Get Pre-Approved

For buying or refinancing a home

- Recent pay stubs

- W-2s or tax returns (typically 2 years)

- Bank statements (checking, savings, retirement)

- Social Security number (for credit review)

- A valid ID (driver’s license or similar)

- Current mortgage details (if refinancing)

These help verify employment, income, assets, and your ability to repay the loan.

For investment properties

- Property income details (lease, rent roll, or projected rents)

- DSCR details (we can help calculate it)

- Rehab budget (for Fix & Flip financing)

- LLC or entity documentation (if applicable)

- Personal or business bank statements

Investors can also run quick estimates using the Fix & Flip Calculator or DSCR Rental Calculator.

When Should You Get Pre-Approved?

If you’re serious about buying—or even browsing—getting pre-approved early keeps you ready. Your pre-approval is commonly valid for 60–90 days and can be refreshed if you’re still searching.

- Starting your home or investment search?

- Touring homes next weekend?

- Planning to refinance soon?

Now is the time. Getting ahead of it gives you options—and keeps you from rushing later.

How the Pre-Approval Process Works at VP Capital Lending

- Start your application online It takes just a few minutes.

- View your personalized options See your max loan amount, estimated payment, and loan path based on real data—not guesses.

- Download your pre-approval letter Use it to tour homes, make offers, and show sellers you’re ready.

Want speed + clarity?

Pre-approval puts you in position to act when the right opportunity shows up.

Run Quick Numbers

If you want a fast estimate before applying, these tools can help you get a feel for payments, cash flow, and equity. Then, when you’re ready, you can turn estimates into real numbers with a pre-approval.

When you’re ready for exact terms and a pre-approval letter, the application is the next step.

Turn Estimates Into a Pre-ApprovalCommon Pre-Approval Questions

Buying or Refinancing a Home

How long does pre-approval last?

Does getting pre-approved hurt my credit?

Can I get pre-approved with lower credit?

Can I get denied after being pre-approved?

Investment Properties

Do you pull my credit for investment property pre-approval?

Can I get pre-approved for a rental property without tax returns?

Do I need to buy investment property under an LLC?

What credit score do I need for investment loans?

How do you calculate loan amounts for DSCR or Fix & Flip loans?

Fix & Flip: we factor in purchase price + renovation budget. Use the Fix & Flip Calculator to estimate profit and funding needs.

Ready To Get Pre-Approved?

Whether you’re buying, investing, or refinancing—pre-approval is the first real step toward turning your plan into a closing date.

VP Capital Lending is here to guide you from pre-approval to closing day—whether it’s your first home or your fifth investment.