If you’re a real estate investor—or thinking about becoming one—you’ve probably asked: “How can I grow my portfolio without my personal income being the bottleneck?” That’s exactly where a DSCR loan shines.

Wondering if your property qualifies? Use our DSCR Calculator to check rent, expenses, payment, and DSCR in minutes.

What exactly is a DSCR loan?

A DSCR loan is designed for income-producing real estate. Instead of underwriting you primarily on personal income and DTI, the lender looks at whether the property’s cash flow can support the debt.

The simple idea

If the property’s rental income can cover the mortgage payment (and required expenses), the deal is easier to approve—even for self-employed investors or borrowers with complex tax returns.

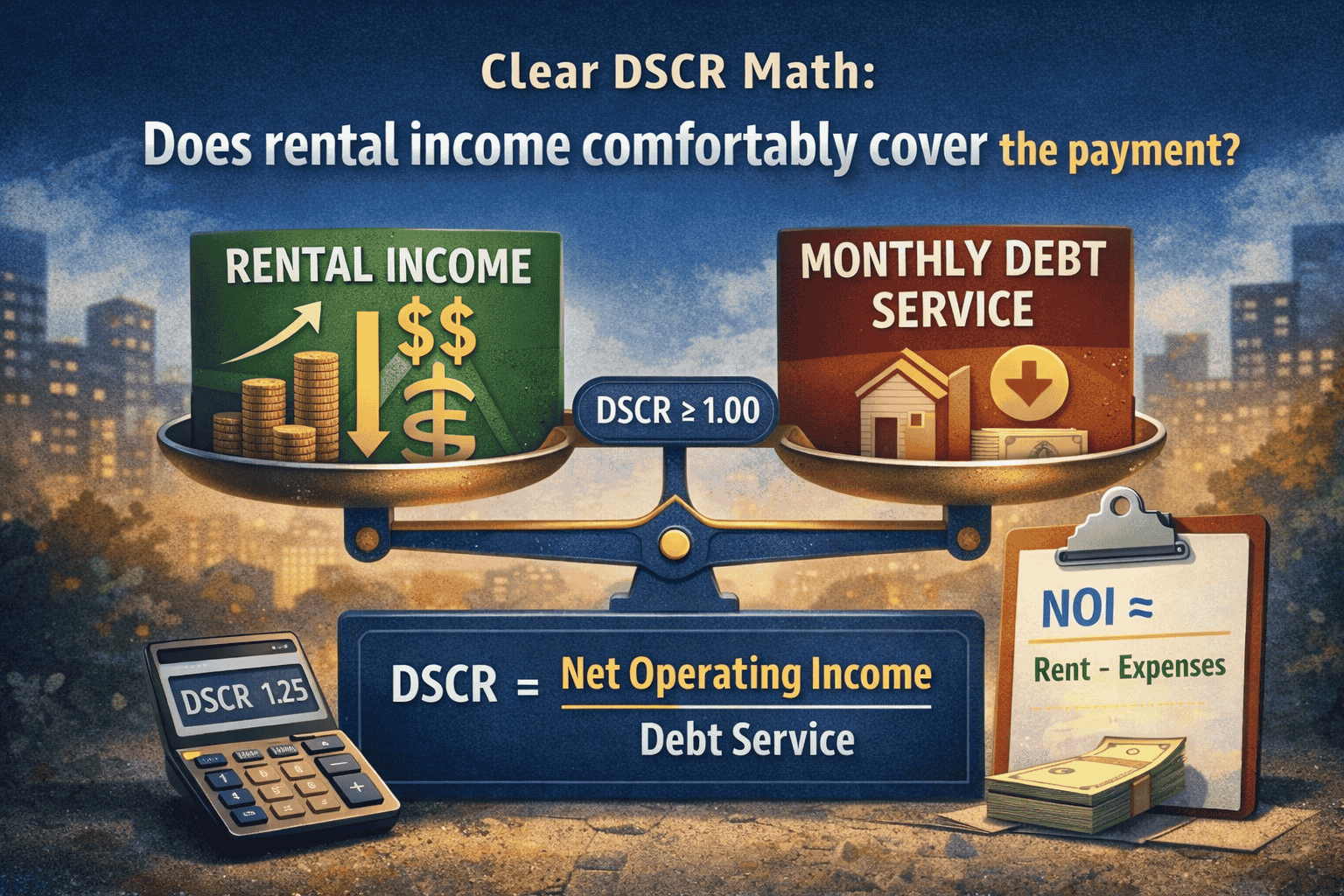

DSCR formula + what the numbers really mean

DSCR is a ratio that answers one question: Does this rental produce enough income to comfortably cover the payment?

Example: DSCR of 1.00

If DSCR is 1.00, the property produces just enough income to cover the required debt service. It’s “break-even” from a lender viewpoint.

Example: DSCR of 1.20

A DSCR of 1.20 means the property produces about 20% more income than what’s needed to cover the debt service—stronger cushion, usually easier approval.

Plug in rent + taxes + insurance + expenses and we’ll calculate payment and DSCR for you.

Check my DSCR →Every lender defines inputs a little differently. That’s why using a consistent calculator—and verifying with your lender—matters.

Why investors love DSCR loans

DSCR loans are popular because they align underwriting with how investors think: the deal should pay for itself.

-

1

No traditional income headache

Many investors are self-employed, write off income, or have uneven earnings. DSCR loans keep the focus on the property.

-

2

Built for scaling multiple properties

Once you start stacking rentals, traditional DTI approaches can get restrictive. DSCR loans can be a cleaner path as your portfolio grows.

-

3

Works well for acquisitions and refinances

Investors use DSCR for purchases and for refinancing stabilized rentals—especially when the goal is better cash flow or pulling equity for the next deal.

-

4

Deal-first decision making

A DSCR approach encourages disciplined buying: if the rents don’t support the payment, it’s a riskier deal—period.

How do you qualify for a DSCR loan?

Guidelines vary by lender and scenario, but these are the most common approval buckets investors should understand.

- DSCR ratio: many programs prefer 1.10–1.25+ depending on structure and pricing.

- Rent support: current lease, rent roll, or market rent (often supported by appraisal/rent schedule).

- Down payment / equity: commonly 20–25%+ on purchases; refinances depend on LTV and scenario.

- Credit profile: stronger credit often improves pricing and approval flexibility.

- Reserves: some programs require liquid reserves (months of payments) based on risk and property count.

How DSCR loans fit into the BRRRR strategy

If you’re using BRRRR—Buy, Rehab, Rent, Refinance, Repeat—the refinance stage is the engine that recycles your capital. A DSCR refinance is often a clean way to move from a rehab loan into long-term rental financing once the property is stabilized.

Common BRRRR flow

- Buy + Rehab with Fix & Flip financing

- Rent the property (stabilize income)

- Refinance into a DSCR loan

- Repeat and scale your portfolio

Why investors prefer DSCR here

Because approval is driven by rental performance, the refinance can be smoother—especially for investors who don’t want traditional income documentation slowing down growth.

Read the BRRRR guide →Common DSCR pitfalls to avoid

Underestimating expenses

If you only look at rent vs mortgage, you can get surprised by taxes, insurance, HOA, and operating costs. Always run the full picture.

Buying based on “hope rent”

Base your numbers on realistic market rent. If projected rent is aggressive, DSCR can miss and the deal becomes hard to structure.

Forgetting rent seasonality

A deal that barely qualifies in a strong month can feel tight if rents soften. Aim for cushion when possible.

Not planning for stabilization

If you’re coming out of rehab, your refinance timing matters. Make sure your rent plan and documentation path support the refinance window.

DSCR ready-check: is your deal a fit?

- ✅ Rent is supported by realistic comps (not best-case guesses).

- ✅ You included taxes + insurance (and HOA if applicable).

- ✅ You accounted for operating expenses (management, maintenance, etc.).

- ✅ The DSCR leaves cushion (not razor-thin).

- ✅ Your plan fits your timeline (purchase vs refinance, rehab vs stabilized).

FAQs about DSCR loans

Can I use a DSCR loan for a new property with no rental history?

Often, yes. Many lenders allow market rent documentation (commonly supported by appraisal or rent schedule) when a property is new to you or not currently leased.

What property types can DSCR loans finance?

DSCR loans commonly finance single-family rentals and small multifamily properties. Eligibility depends on program guidelines and scenario.

Do DSCR loans require tax returns?

Many DSCR programs minimize or avoid traditional income documentation because the property cash flow is central to underwriting.

What DSCR ratio do I need?

It depends on the program, the deal, and pricing. Many structures prefer a stronger ratio (often 1.10–1.25+), but the best first step is running your numbers.

What’s the fastest way to check if my deal qualifies?

Use the DSCR Calculator. It’s the quickest way to model rent, payment, expenses, and DSCR in one place.

Your next steps

Disclaimer: This article is for educational purposes only and does not constitute a commitment to lend. DSCR guidelines, terms, and availability vary by program, property type, and borrower profile.