Investor Financing Guide

DSCR (Debt-Service Coverage Ratio) is one of the most important numbers in rental lending. It tells lenders whether your property’s income can comfortably cover the monthly payment and expenses. This guide breaks DSCR down step-by-step with clear formulas, lender-style calculations, and real examples—so you can analyze deals faster and finance with confidence.

Quick DSCR Snapshot

Most common investor definition

Many programs use a similar approach, but the exact inputs can vary by lender. We’ll cover the variants below.

Quick tip: Don’t want to do the math manually? Run your numbers with our DSCR Calculator and see your ratio in seconds.

What DSCR means

How lenders interpret risk and approval thresholds.

How to calculate DSCR

A simple step-by-step method with clean formulas.

Real examples

See DSCR in action (and how small changes move it).

BRRRR connection

Why DSCR matters most during the refinance stage.

What Is DSCR?

DSCR stands for Debt-Service Coverage Ratio. It measures how easily a rental property can cover its monthly “debt service” (the payment) based on the income the property produces.

Think of DSCR as a safety cushion. A DSCR of 1.20 means the property generates about 20% more income than it needs to cover the required monthly obligations in the lender’s DSCR model.

DSCR in plain English

“Does this property bring in enough money each month to safely cover the payment (and sometimes expenses)?”

DSCR isn’t personal DTI

DSCR focuses on the property. That’s why DSCR programs are popular with investors who don’t want W-2 income or complex DTI calculations driving approval.

Why DSCR Matters for Real Estate Investors

Lenders use DSCR to evaluate risk. The stronger your DSCR, the more comfortable a lender is that the property can handle the payment—even if you have vacancies, repairs, or market shifts.

- Approval: Many DSCR programs require a minimum DSCR to qualify.

- Pricing: Better ratios can improve rate/terms in many investor programs.

- Scaling: Higher DSCR often makes it easier to buy the next property (especially with BRRRR).

Important: DSCR calculations vary by lender and product. Two lenders can look at the same property and calculate different DSCR values depending on what they include as “debt service” and “expenses.”

DSCR Formulas Lenders Use (And Why They Differ)

You’ll see DSCR described in different ways. The concept is always the same: income ÷ required monthly obligation. What changes is which income and which obligations are counted.

Formula A: NOI-based DSCR (classic finance definition)

This is common in commercial real estate. It’s clean—but many DSCR rental programs don’t use NOI exactly this way.

Formula B: Rent-based DSCR (common in DSCR rental lending)

Many investor DSCR programs focus heavily on rent versus the monthly payment (often including taxes/insurance). Some also include HOA, management, and maintenance allowances.

In this guide, we’ll show you the most practical investor method you can use to screen deals: Gross Rent ÷ (Estimated Payment + Monthly Expenses)—and we’ll also explain where lender models may differ.

Step-by-Step: How to Calculate Your DSCR

Here’s the simplest way to calculate DSCR for rental property analysis. You’ll do three things: (1) total monthly income, (2) total monthly obligations, then (3) divide.

Start with gross monthly rent

Use the property’s current lease rent when available. If it’s a new purchase or rent is uncertain, many lenders use market rent from the appraisal (rent schedule).

Pro move: be conservative. If the market is soft or you’re budgeting renovations, don’t inflate rent projections.

Calculate the estimated monthly payment (PITI)

Your estimated payment typically includes principal + interest, and many lender models also include taxes + insurance. If there’s an HOA, include it as well when relevant.

Shortcut: If you’re using our calculator, it estimates the monthly payment and then lets you add common monthly expenses—so you can see DSCR without spreadsheets.

Add monthly operating expenses used in your model

For practical deal screening, include recurring items like maintenance, management, HOA, and misc expenses. (We’ll cover what counts below.)

Divide income by obligations

Once you have rent and monthly obligations, DSCR is simply:

If DSCR is 1.00, the property is breaking even in the model. Above 1.00 is stronger. Below 1.00 is typically a red flag for financing.

What to Include in DSCR Calculations (Income + Expenses)

DSCR is only as accurate as the inputs you choose. Below is a practical, investor-friendly way to think about the numbers—plus the items that commonly trip people up.

Income to use

- Monthly rent: in-place lease rent when available

- Market rent: often supported by appraisal rent schedule

- Other income (case-by-case): sometimes parking/storage/laundry (ask your lender)

Monthly obligations commonly included

- Principal & interest (P&I)

- Taxes + insurance (often included in DSCR models)

- HOA (if applicable)

- Maintenance (budgeted monthly)

Be careful with “future” rent. If the property needs repairs before it can hit your target rent, many lender models won’t give full credit until it’s supported.

What NOT to include (common confusion)

- Down payment (it affects the loan amount/payment, but it’s not a monthly operating expense)

- One-time repairs (unless you’re turning them into a recurring monthly reserve)

- Appraisal, closing costs, and lender fees (not part of DSCR math)

- Vacancy (some lenders apply a vacancy factor; your personal model can, too—just be consistent)

What DSCR Do Lenders Want?

Minimum DSCR varies by lender, product, and scenario. But here’s a practical way to interpret your ratio during deal analysis.

| DSCR | What it usually means | How investors use it |

|---|---|---|

| < 1.00 | Income doesn’t fully cover obligations in the model. | Often a hard stop unless structure/terms change. |

| 1.00 – 1.09 | Break-even to slightly positive. | May be challenging depending on lender; tighten expenses or improve rent. |

| 1.10 – 1.19 | Generally acceptable for many investor scenarios. | Solid “workable” DSCR range for scaling. |

| 1.20+ | Strong cushion. | Often considered “healthy,” can improve options and confidence. |

Pro tip: If you’re close to a threshold (like 1.10), small adjustments can matter: a slightly lower rate, a modest rent increase, or trimming recurring expenses can push DSCR over the line.

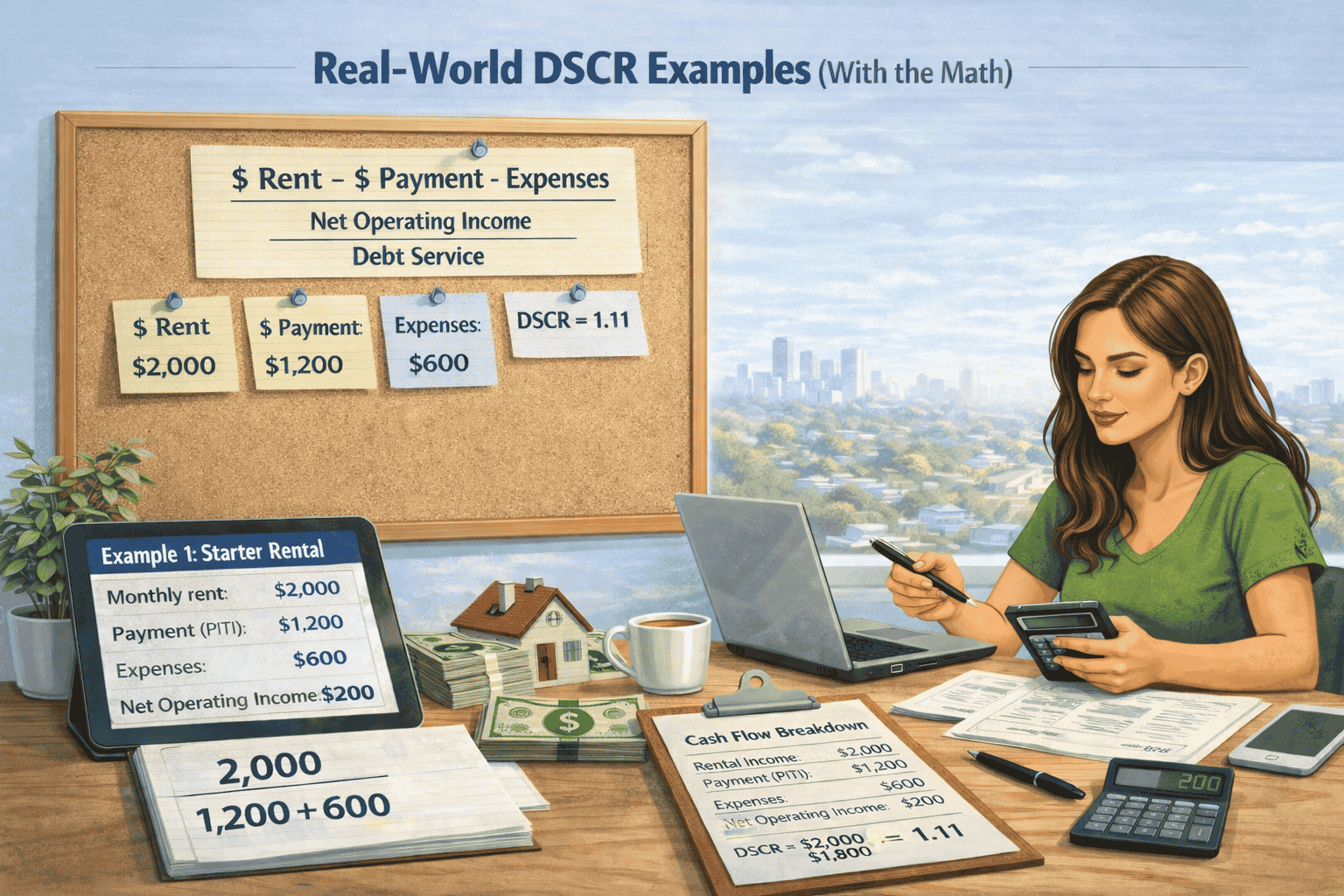

Real-World DSCR Examples (With the Math)

Example 1: The “clean” starter rental

Monthly rent

$2,000

Estimated payment (PITI)

$1,200

Monthly expenses

$600

DSCR = 1.11

This property has a modest cushion. If your lender minimum is 1.10, you’re above the line—but you’d still want to watch taxes/insurance changes and any expense creep.

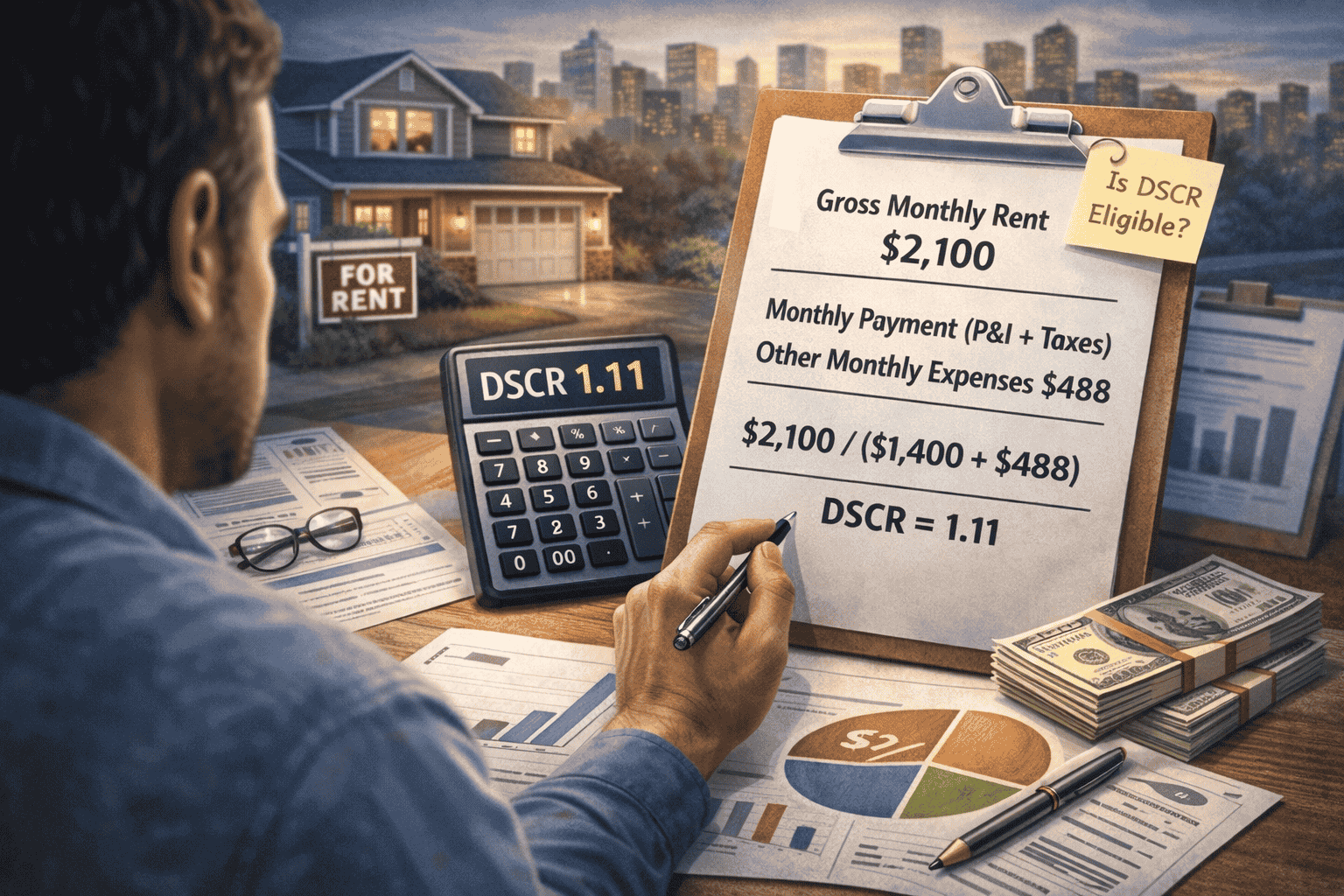

Example 2: Sophia’s deal analysis (real-world scenario)

Meet Sophia. She’s analyzing a rental in a strong area and wants to confirm it clears DSCR requirements.

Monthly rent

$2,250

Estimated payment (PITI)

$1,400

Monthly expenses

$488

DSCR = 1.19

If the program minimum is 1.10, Sophia is eligible on DSCR. If the program targets 1.20, she’d need a better payment structure or stronger income.

Example 3: How small changes can flip the decision

If you’re close to the minimum, the fastest way to improve DSCR is usually the monthly payment.

- If payment drops from $1,400 to $1,325 (rate/structure change), DSCR improves.

- If rent increases from $2,100 to $2,200, DSCR improves.

- If expenses get reduced by $50–$100/mo, DSCR improves.

This is why a quick calculator is so useful during deal screening.

How to Improve DSCR (Without Guessing)

DSCR has only two levers: increase income or reduce monthly obligations. Here are the practical moves investors use most.

Increase income (responsibly)

- Confirm market rent with comps (don’t “hope” your way to DSCR)

- Add value: minor upgrades that justify rent premiums

- Reduce vacancy: better tenant screening and turnover planning

- Consider additional allowable income (where supported)

Reduce monthly obligations

- Lower rate via better credit/profile or timing

- Adjust leverage (loan amount/LTV impacts payment)

- Choose a structure that fits the property (term, IO options where available)

- Shop insurance and verify tax estimates (these can move DSCR a lot)

Watch taxes and insurance. Even if your principal and interest looks great, higher-than-expected taxes/insurance can lower DSCR and surprise investors after closing.

How DSCR Fits Into the BRRRR Strategy

If you’re using the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat), DSCR matters most during the refinance stage—because lenders will look at the stabilized rent and monthly obligations to determine eligibility and terms.

Why it matters during refinance

- A stronger DSCR can expand refinance options and improve terms.

- Better DSCR can help you pull equity more safely (depending on your goals).

- If DSCR is tight, you may need to adjust rent, expenses, or structure before refinancing.

Want the full BRRRR financing workflow?

Read our guide on using Fix & Flip financing to buy + rehab, then refinancing into DSCR long-term rental financing.

Common DSCR Mistakes That Cost Investors Deals

- Using optimistic rent: your “target rent” isn’t always lender-supported rent.

- Ignoring taxes/insurance: they can swing DSCR dramatically.

- Mixing models: comparing lender DSCR to your NOI DSCR without realizing they’re different.

- Forgetting HOA/recurring fees: small monthly charges add up.

- Not stress-testing: no buffer for vacancy, repairs, or rent softness.

If you want to be conservative, try a quick “stress test”: reduce rent by 5% or add a small monthly reserve—then see whether DSCR still clears your target.

FAQs About Calculating DSCR

Can DSCR vary by property type?

Yes. Multi-family properties can have higher operating costs (maintenance, turnover, utilities in some cases), and HOA/condo fees can also impact obligations—both of which can affect DSCR.

What’s the minimum DSCR I need for approval?

Many investor programs look for DSCR around 1.10+, while others prefer 1.20+. Requirements vary by lender, property type, and scenario.

Do lenders use actual rent or market rent?

It depends. If there’s an in-place lease, some lenders use it. Other times (especially for new acquisitions), lenders may use the appraisal’s market rent/rent schedule. When in doubt, run both scenarios.

Should vacancy be included in DSCR calculations?

Some lender models apply a vacancy factor, and many investors do as part of conservative underwriting. If you include vacancy, stay consistent across deals so your comparisons remain apples-to-apples.

Is DSCR the same as cash flow?

Not exactly. DSCR is a ratio lenders use for risk and approval. Cash flow is your actual leftover money after all expenses and reserves. A deal can “pass DSCR” and still feel tight on real cash flow if expenses are underestimated.

Your Next Steps

Once you understand DSCR, you can screen deals faster, structure financing more intelligently, and avoid surprises during underwriting. If you’re analyzing a purchase or preparing for a refinance, DSCR gives you a real edge.

What to do next

- Use our DSCR Calculator to run your numbers quickly.

- Learn how DSCR supports BRRRR-style investing (especially at refinance).

- Ready to move forward? Start your approval or contact us to sanity-check structure and terms.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. DSCR calculations and underwriting guidelines vary by lender and program. For an accurate scenario review, talk with a loan advisor.